Site Content

Click Here for INL News Amazon Best Seller Books

INLTV Uncensored News

INLTV is Easy To Find Hard To Leave

Quality New Homes FOR SALE near Navan, Meath, Ireland f€1000 Euros Deposit

All enquiries: admin@y-realtor.com

These Quality New Homes with 2, 3 and 4 bedrooms are being built near Navan in Meath Ireland which can be purchased from €1,000 Euros Deposit

Market Square Navan, Meath, Ireland

These top quality new homes which will include a substantial allowance for furniture, floor coverings, fixtures and fittings

Navan is the county town of County Meath, Ireland. One can get to Dublin by bus or drive from Navan to Dublin under one hour, which makes anyone living near Navan can commute to work in Dublin, the capital city of Ireland.

In 2016 Navan had a population of 30,173, making it the tenth largest settlement in Ireland.

Navan is at the confluence of the River Boyne and Blackwater, around 50 km northwest of Dublin. Navan is a Norman foundation: Hugh de Lacy, who was granted the Lordship of Meath in 1172, awarded the Barony of Navan to one of his knights, Jocelyn de Angulo, who built a fort there, from which the town developed.

UNIQUE FRENCH OCEAN VIEW PROPERTY- SAINT-TROPEZ • €34,500,000 This unique private 5800m² property

UNIQUE FRENCH PROPERTY- SAINT-TROPEZ • €34,500,000As an aside, The Daniel FÉAU Private Collection: In absolute calm, in the immediate vicinity of the heart of Saint Tropez, global renovation / construction project of several houses or hamlet, for a total area of 740m² of living space on a quality plot of 5800m².

The project includes:

A house to renovate of 360m ² living space enjoying a sea view, a second house (friends or caretaker) of 100m ² to renovate also and two building permits obtained for two new villas totaling 260m2 of additional living space.

This unique rare as hens teeth property is a once in a life time opportunity to purchase a global develop project in the most sort after ocean front area in France. We can advise you architect and project manager. Extremely rare and qualitative set for huge long term capital growth.

Be quick to make your best offer before another shrewd investor out bids you.

Further Details on

UNIQUE FRENCH PROPERTY- SAINT-TROPEZ

Reference: 7951985

Area: 747 m²

Orientation: South-west

View: Unobstructed Sea

Waste water: Septic tank

Heating: Fuel oil Central Individual

SERVICES

Swimming pool, Fireplace, Intercom, Electric gate.

All enquires June Cambell

Email: admin@y-realtor.com

Elon Musk takes control of Twitter in $44bn deal

By James Clayton & Peter Hoskins

BBC News 28 October 2022

Yahoo Real Estate Pty Ltd receives One Billion offer for 51% of its domain name www.YTweet.org from Amit Ashram, which backed by an Indian Investment Group who want to take on Twitter just purchased by Elon Musk for $44 billion, to create an "independent uncensored voice" for everyone on planet earth

The world's richest man, Elon Musk, has completed his $44bn (£38.1bn) takeover of Twitter, according to a filing with the US government.

Mr Musk tweeted "the bird is freed" and later said "let the good times roll".

A number of top executives, including the boss, Parag Agrawal, have reportedly been fired. Mr Agrawal and two other executives were escorted out of Twitter's San Francisco headquarters on Thursday evening, said Reuters.

With Y-Realtor you can help you buy-sell-trade-swap, or rent your property, land or business and give whatever advise you need relating to your real estate needs. At Y-Realtor.com we take pride in helping a property and business owner obtain the best price or rent. Sometimes an option to trade or swap for another asset can be considered as a great option. This can be done by trading up or down in value. At Y-Realtor.com we advise on the alternative finance options when purchasing a property or business. We also at Y-Realtor.com help purchasers and renters find the property or business they want to buy, trade, swap or rent.

Real Estate 2022: The rise of rent, home prices, mortgage rates and inflation

Buy or build a house: What’s cheaper? 2022 Cost comparison

Peter WardenThe Mortgage Reports EditorJuly 19, 2022 - 9 min read

Peter WardenThe Mortgage Reports EditorJuly 19, 2022 - 9 min read

Should you build or buy a home?

With home price inflation continuing its upward path, many would-be buyers are considering alternatives — like building their own house from scratch rather than buying an existing one.

But that begs the question, is it cheaper to build or buy a house?

If you compare average build prices to average purchase prices, building your own home is generally more expensive. But there are so many variables that this is far from certain in every case.

Wondering whether to build or buy in 2022? Here’s what you should know.

Verify your home loan eligibility. Start here (Aug 29th, 2022)

In this article (Skip to...)

Is it cheaper to build or buy a house?

As a rule of thumb, it’s cheaper to buy a house than to build one. Building a new home costs $34,000 more, on average, than purchasing an existing home.

The median cost of new construction was $449,000 in May 2022. Comparatively, the median cost to buy an existing home was $414,200, according to the most recent data available from the National Association of Home Builders (NAHB) and the U.S. Census Bureau.

- Average cost to build a house: $449,000

- Average cost to buy a house: $414,200

The cost of building a new house includes buying a plot, excavations, permits, inspections, and other associated costs.

However, the data reveals a significant drop in costs for those who already have a lot on which to build. A separate study from the NAHB, dating back to 2019, ballparks the purchase price for a plot to be 18.5% of the total costs for new construction. This bumps down the cost of building a home to an estimated $365,935 for those who already own a lot.

So, which is the right choice? That depends on many factors — like your needs, location, timeline, local home inventory, and the availability and prices of materials and labor.

Let’s dig into these factors a little further to help you weigh the costs and benefits of building versus buying.

Check your home buying options. Start here (Aug 29th, 2022)

Average cost to build a house

NAHB put the average cost to build a house at $449,000 in May of 2022. That’s including the cost to buy a plot of land.

With the land purchase included, there’s an 8% gap between the average price of building and buying. And building could end up being substantially more expensive depending on your location, construction plans, and the cost of materials and labor.

What impacts the cost of building a home

First is the cost of construction. This can vary a lot not only by the home builder, but also depending on the cost of materials and when you want to build.

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot or much more if you want the best of everything.

If you have the time and skills to do some of the construction work yourself, that might bring big savings. Just don’t try to do work that’s beyond your capabilities. There will be independent inspections and the home must be mortgageable to have a sensible resale value.

Then there’s the location.

HomeAdvisor reports that it can cost more than twice as much to build in Alaska as in Kansas. And between those two extremes, range the costs in all the other states.

Other building costs to consider

Other variables in the building process include:

- Site costs: Home builders have multiple site fees, including those for building permits, water and sewage inspections, and architectural and engineering plans, to name a few

- Foundation: A new home with a basement will increase the overall costs. But even without one, you’ll still pay for excavation, foundation, concrete, and retaining walls

- Framing and exterior finishes: Not only do these costs vary depending on the square footage of the home and its floor plan, but you’ll also need to figure in the price for building materials and labor costs (such as your general contractor and any subcontractors)

- Major home systems: These include plumbing, electrical, and HVAC. Again, labor costs for plumbers and electricians also apply

- Interior finishes: Don’t forget your custom home’s flooring, drywall, countertops, appliances, and other amenities

- Plot: Landscaping, outdoor structures, decks, driveways, and cleanup costs

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot if you want the best of everything.

And, no doubt, you could easily bust that top figure if you choose to import acres of Calacatta Carrara marble from Italy for your 5,000-square-foot home.

Plan for overruns

Of course, some construction projects sail through on time and on budget. But it’s very common for both to overrun. So you should build in a 5% or 10% contingency to take care of unexpected building costs. And more if you’re the sort of person who’s easily tempted to overspend when confronted with a range of choices.

Financing a new construction home

Yet another variable is your financing plan. Some people use a mortgage to buy the land and then use savings or a construction loan to fund the project.

But then, when the work is finished, you’ll usually have to refinance the mortgage to repay the bank or replenish your savings. And that means two sets of closing costs: One for the original land purchase loan and another for the refinance.

Meanwhile, construction loans typically come with higher interest rates than standard mortgages. Additionally, there are strict rules about the timeline for construction and disbursement of funds.

An alternative is to get a construction-to-permanent loan. With one of these, you borrow using a single loan to buy the land and build the home. Money is released as you reach preset construction milestones.

For more information, read: Financial steps to building a house: The complete guide

Average cost to buy a house

In May 2022, the median home sales price for an existing house was $414,200 according to the NAHB and U.S. Census Bureau.

But, just as construction costs vary by state, so do home prices. Indeed, there can be enormous differences within states by city, county, and neighborhood.

For example, buy a home in Ilion, New York, and you can expect housing costs that are roughly 800% less than the statewide average. But purchase one in Chelsea, NYC, and you can expect to pay dearly. The median sale price there in April 2022 was an astronomical $2 million, according to Realtor.com.

Home price inflation

There’s yet another component in your decision-making process. How quickly are home prices rising where you want to buy or build?

In June 2022, CoreLogic reported that home sales prices nationwide, “increased year-over-year by 20.9% in April 2022 compared with April 2021.” That’s an annualized figure, meaning home prices in April 2022 were 20.9% higher than they were 12 months earlier. Furthermore, no states reported an annual decline in home values.

Again, that’s a nationwide average. If you’re a first-time buyer, home prices where you want to live may well have risen more gently. But it’s just as likely they’ll have shot up even more sharply.

For example, if you wanted to buy in Arizona, Florida, or Tennessee, CoreLogic says prices in all three states rocketed by more than 27% over those 12 months. That might influence your decision over whether to build or buy your home.

Consider your timeline

Should you divert some of your down payment savings into buying a plot now? You could then sit on it until you can afford to begin construction on your dream home. That way, you’d have control over at least some of your housing costs. Indeed, you could argue you have a foot on the bottom rung of the housing ladder.

So to truly answer the question of whether it’s cheaper to build or buy a house, you’ll need to do a lot of homework.

In fact, you may not be entirely sure until you’ve found the plot you want, obtained estimates from contractors, and compared those costs to similar existing homes in the neighborhood.

Verify your home loan eligibility. Start here (Aug 29th, 2022)

Buying a new home vs. existing home

There’s one more option. And that’s to buy a new-build home, which is a new house that was only just constructed, but that you didn’t have built for yourself. There are benefits and drawbacks to this strategy as well.

Back in 2017, Trulia estimated that homebuyers paid a premium of about 28% when they bought a new home.

So it might cost you $512,000 to buy a new home that’s comparable with a $400,000 existing home ($400,000 + 28% = $512,000).

Trulia’s article had the headline, “What You’ll Pay for That New Home Smell.” And it’s true that the smell is nice, as is the prestige that a newer home brings. Better yet, you’ll probably have the latest of everything: technologies, finishes, construction techniques, and more.

Home warranties and other savings

There are also solid financial perks to owning a brand new home. For example, you’re way less likely to face unexpected upgrades and expensive renovations.

If you do, those repairs may be covered by the builder’s warranty. NOLO, a legal website, suggests such warranties commonly provide the following protections:

- One year on labor and materials

- Two years on mechanical defects (air conditioning, electrical, heating and ventilation systems, and plumbing)

- Ten years on structural defects in the home

Of course, if you’re using general contractors to build your own new home, you’ll have to negotiate warranties with them.

So you stand to make savings on home repairs by buying new. But there can be other financial benefits. You’ll typically have better insulation than an older home provides and may have more energy-efficient systems and appliances. And all that should deliver lower utility bills, besides helping you do your bit for the planet.

True, it’s hard to assign dollar values to your likely savings. But you should take them into account when deciding on whether or not it’s more expensive to buy or build your own home.

Is it cheaper to buy or build a house in today’s market?

So far, we’ve explored the general principles in the buy-versus-build contest. But what differences do the current economy and property market make?

This article was written as global forces such as supply-chain issues and inflation were pushing construction costs sky-high, when making predictions was even more difficult than usual. But here are some factors that might swing your take on whether it is better to build or buy a house in 2022 and beyond:

- Inventory shortage: There are just too few homes available to satisfy demand. That’s unlikely to change for years because the only way out is to build more homes. It could take years or more than a decade to build enough

- Shortage of labor to build: 2021 and 2022 were unusual years for employment. Some older Americans retired early, and record numbers of young people dropped out of employment to start their own businesses. So the construction industry had a hard time putting boots on plots and paying higher wages to attract workers

- Current material costs: The Covid-19 pandemic caused lingering supply chain issues that created shortages in many products, including construction materials. Take lumber as an example. According to the NAHB, “Extremely volatile lumber prices during the past year have caused the average price of a new single-family home to increase by more than $18,600.” Will building material prices keep falling or head higher in the near future? Only time can tell

There are challenges to consider in the existing-home market, too.

Rising Construction Costs Impact Everyone in the Property Market

12th Apr, 2022

https://ybr.com.au/rising-construction-costs-impact-everyone-in-the-property-market/

Construction costs are on the rise in Australia. So what can you do to protect yourself from rising construction costs?

It’s no secret that construction costs are on the rise in Australia. In fact, a report from CoreLogic showed that national construction costs increased by 7.3% over the 2021 calendar year. This rate of increase is the highest annual growth in construction costs since March 2005.

This is great news for the construction industry, but it could spell trouble for homeowners who are planning to renovate or build their new homes. So what can you do to protect yourself from rising construction costs? We’re going to cover why we’re seeing increasing costs for construction and what you need to be aware of.

Increased costs:

There are various factors contributing to increased costs of construction, but the most notable factors include:

- An increase in the cost of supplies like structural timber and metal products.

- A skill shortage in the construction industry. There are difficulties with importing skilled workers, meaning the cost of local labour is on the rise, particularly as the demand for renovations and tradespeople continues to rise.

CoreLogic Research Director Time Lawless said, “There is a significant amount of residential construction work in the pipeline that has been approved but not yet completed.”

“With some materials such as timber and metal products reportedly remaining in short supply, there is the possibility some residential projects will be delayed or run over budget.”

“With such a large rise in construction costs over the year, we could see this translating into more expensive new homes and bigger renovation costs,” said Mr Lawless.

Who does this impact?

The rise in construction costs could have substantial impacts on the residential property market. CoreLogic Head of Insurance Solution, Matthew Walker, warned that all homeowners and property investors could be impacted, not just homeowners looking to renovate or business owners.

“In these times of rapidly rising home and construction costs, under insurance can quickly become a real threat to what is a most valuable asset. It’s important that homeowners keep track of their sum insured and annually check that it is sufficient should the worst occur by using their insurer’s rebuild calculator or giving them a call,” said Mr Walker.

It’s not just a shortage in skilled workers and essential building materials contributing to rising costs but also market demand. Australia has been on a ‘home building boom’,

How to protect yourself if you’re looking to build your home or renovate

There are generally two types of contracts when you engage a builder for a construction project. It’s particularly important to be aware of these contracts if you’re looking to take out a construction loan through your lender or mortgage broker. If you’re aware of these two contract types, you may be able to better protect yourself from rising construction costs.

Generally speaking, there are two types of construction contracts:

- Fixed price building contracts

This is the type of construction contract most lenders will insist on, as it clearly defines the scope of your agreement with your builder: the price you pay is agreed, even if prices for things like building materials increase during the construction project.

Generally, an experienced builder will add a margin for pricing changes, so you can expect to pay a little extra here, however, you are protecting yourself from the shock of any significant price increases for materials like timber or steel.

You can find guidance on these contracts at Fair Trading NSW, which provides a checklist of what to be wary of.

- Cost-plus contracts

The other type of contract generally used is referred to as a cost-plus contract.

These contracts have some benefits if you don’t mind the administrative work associated with them. With these contracts, you’re not locked into a fixed price. If prices for materials like structural timber or metal products increase during the course of the construction project, the cost of your project will increase as well. This process allows you as the owner of the project to receive invoices for each expense incurred from your builder but can create a situation where the builder has less incentive to save costs during the build as they are not necessarily working within an agreed quote. If you don’t personally mind the extra workload of monitoring costs and staying up to date with progress payments throughout your construction project, this contract may work for you.

However, you need to be aware that if you require a construction loan to proceed with your project, most lenders generally refuse to accept applications based on cost-plus contracts. Under these contracts, the entire risk, should materials increase in cost, is passed onto you.particularly after the federal government’s HomeBuilder scheme.

Filming of the first feature film soon to start at 93 Cambridge in Mitchell Queensland, Australia

INL News Amazon Best Seller Books

<a target="_blank" href="https://www.amazon.com/b?_encoding=UTF8&tag=inlnewsgroup-20&linkCode=ur2&linkId=e20517e1dc7b74735db362fc2748bf0b&camp=1789&creative=9325&node=283155">INL News Amazon Best Seller Books</a>

93-95 CAMBRIDGE STREET, Mitchell, Qld 4465

Click menu above for all items (inltv.co.uk)

$2,750,000 Offer made for 93 Cambridge Street, Mitchell, Queensland, Australia; 4465

THE WESTERN HOTEL OR A HUGE COUNTRY HOME!93-95 CAMBRIDGE STREET, MITCHELL, Queensland, 4465 True Asking Price$2,950,000

Chris Rowe at Accommodation Business Brokers Appointed To Sell The Famous 1860's Historical

Western Hotel at 93-95 Cambridge Street, Mitchell, Queensland, Australia

93-95 Cambridge Street, Mitchell, Queeld, 4465 for sale for $2,950,000

See Below The Western Hotel Advertisements

https://www.commercialrealestate.com.au/property/mitchell-qld-4465-2018039067

https://www.accommodationbusinessbrokers.com.au/business/mitchell-qld-4465-r2-3424066/

https://www.accommodationbusinessbrokers.com.au/agents/chris-rowe/

Chris Rowe has been involved in the Accommodation and Hospitality Industry for many years.

Chris Row has established strong long lasting relationships with his clients.

The shareholders of Yahoo Real Estate Pty Ltd and its film production partners are extremely excited that filming of their first feature film will soon commence at the famous historic Western Hotel 93-95 Cambridge Street, Mitchell, Queensland, Australia, 4465. The Western Hotel was built in 1854 by Thomas Close, who acquired the original Mitchell Downs Homestead from Edmund Murray. in 1864 Thomas Close used the building materials from the Mitchell Downs Homestead to help built and established the Maranoa Hotel, which now known as the Western Hotel. The town of Mitchell is named after Sir Thomas Mitchell, explorer and Surveyor General of New South Wales. Mitchell is a town and locality in the Western Downs District of the Maranoa Region, Queensland, Australia. The town of Mitchell services a very economically strong tourism, cattle and sheep farming district. Before the arrival of Europeans, the Maranoa region was occupied by the Mandandanji and Gunggari Aboriginal peoples. Based on archaeological excavations in the Mount Moffatt area, it has been deducted that the Aboriginals had lived there for around 19,500 years. Descendants of the original peoples still live in and visit the area today. Mandananji (also known as Mandananyi, Mandandanjdji, Kogai) is an Australian Aboriginal language spoken by the Mandandanji people. On 1st January 1865, Mitchell Downs Post Office opened and around 1878 was renamed Mitchell Post Office. The Mitchell State School opened on 1st April 1876.

In 1902, after a short stand-off, bush rangers Patrick and James Kennith were captured south of Mitchell at a location, previously known as Back Creek, but now known as Arrest Creek. Patrick Kennith was hanged in 1903 for the murder of Constable George Doyle and Albert Hahike, while James Kennith was released after 12 years imprisonment and died peacefully in 1940.

The Great Artesian Spa in Mitchell was opened in 1998 and is situated in the town of Mitchell's aquatic centre. The water used in the Great Artesian Spar in Mitchell is renewed regularly and comes from the great Artesian Basin. which is one of the largest artesian basins in the world, which underlies around one-fifth of Australia. It covers a total area of more than 1,711,000 square kilometres, and has been relied upon for Mitchell's town water since 1927.

Other attractions or Mitchell include: The Mitchell Yumba Interpretive Trail, the Neil Turner Weir, the Kennith Courthouse, Kennith Brothers sculpture at Arrest Creek, Major Mitchell's Campsite 38 Kilometres north of Mitchell, Musical Cattle Grid on the banks of the Maranoa River, nearby Roma, Surat, Wallunbilla, Yuleba and Injune, Great fishing at Fisherman's Rest on the banks of the beautiful Maranoa River, which has a ramp to allow easy access to the river to launch a boat or kayak and try your luck fishing for yellowbelly and other fish species, tour the Booringa Heritage Museum, packed full of local history, historical items and old photographs, wander the Mitchell on Maranoa Gallery, which is an historic picture theatre that has been transformed into the Mitchell on Maranoa Gallery, enjoy a "Maranoa River Walk", explore the Mt Moffatt Section of the Carnarvon National Park, enjoy a number of tourist drives in the greater Roma Region.

Average cost to build a house

NAHB put the average cost to build a house at $449,000 in May of 2022. That’s including the cost to buy a plot of land.

With the land purchase included, there’s an 8% gap between the average price of building and buying. And building could end up being substantially more expensive depending on your location, construction plans, and the cost of materials and labor.

What impacts the cost of building a home

First is the cost of construction. This can vary a lot not only by the home builder, but also depending on the cost of materials and when you want to build.

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot or much more if you want the best of everything.

If you have the time and skills to do some of the construction work yourself, that might bring big savings. Just don’t try to do work that’s beyond your capabilities. There will be independent inspections and the home must be mortgageable to have a sensible resale value.

Then there’s the location.

HomeAdvisor reports that it can cost more than twice as much to build in Alaska as in Kansas. And between those two extremes, range the costs in all the other states.

Other building costs to consider

Other variables in the building process include:

- Site costs: Home builders have multiple site fees, including those for building permits, water and sewage inspections, and architectural and engineering plans, to name a few

- Foundation: A new home with a basement will increase the overall costs. But even without one, you’ll still pay for excavation, foundation, concrete, and retaining walls

- Framing and exterior finishes: Not only do these costs vary depending on the square footage of the home and its floor plan, but you’ll also need to figure in the price for building materials and labor costs (such as your general contractor and any subcontractors)

- Major home systems: These include plumbing, electrical, and HVAC. Again, labor costs for plumbers and electricians also apply

- Interior finishes: Don’t forget your custom home’s flooring, drywall, countertops, appliances, and other amenities

- Plot: Landscaping, outdoor structures, decks, driveways, and cleanup costs

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot if you want the best of everything.

And, no doubt, you could easily bust that top figure if you choose to import acres of Calacatta Carrara marble from Italy for your 5,000-square-foot home.

Plan for overruns

Of course, some construction projects sail through on time and on budget. But it’s very common for both to overrun. So you should build in a 5% or 10% contingency to take care of unexpected building costs. And more if you’re the sort of person who’s easily tempted to overspend when confronted with a range of choices.

Financing a new construction home

Yet another variable is your financing plan. Some people use a mortgage to buy the land and then use savings or a construction loan to fund the project.

But then, when the work is finished, you’ll usually have to refinance the mortgage to repay the bank or replenish your savings. And that means two sets of closing costs: One for the original land purchase loan and another for the refinance.

Meanwhile, construction loans typically come with higher interest rates than standard mortgages. Additionally, there are strict rules about the timeline for construction and disbursement of funds.

An alternative is to get a construction-to-permanent loan. With one of these, you borrow using a single loan to buy the land and build the home. Money is released as you reach preset construction milestones.

For more information, read: Financial steps to building a house: The complete guide

Average cost to buy a house

In May 2022, the median home sales price for an existing house was $414,200 according to the NAHB and U.S. Census Bureau.

But, just as construction costs vary by state, so do home prices. Indeed, there can be enormous differences within states by city, county, and neighborhood.

For example, buy a home in Ilion, New York, and you can expect housing costs that are roughly 800% less than the statewide average. But purchase one in Chelsea, NYC, and you can expect to pay dearly. The median sale price there in April 2022 was an astronomical $2 million, according to Realtor.com.

Home price inflation

There’s yet another component in your decision-making process. How quickly are home prices rising where you want to buy or build?

In June 2022, CoreLogic reported that home sales prices nationwide, “increased year-over-year by 20.9% in April 2022 compared with April 2021.” That’s an annualized figure, meaning home prices in April 2022 were 20.9% higher than they were 12 months earlier. Furthermore, no states reported an annual decline in home values.

Again, that’s a nationwide average. If you’re a first-time buyer, home prices where you want to live may well have risen more gently. But it’s just as likely they’ll have shot up even more sharply.

For example, if you wanted to buy in Arizona, Florida, or Tennessee, CoreLogic says prices in all three states rocketed by more than 27% over those 12 months. That might influence your decision over whether to build or buy your home.

Consider your timeline

Should you divert some of your down payment savings into buying a plot now? You could then sit on it until you can afford to begin construction on your dream home. That way, you’d have control over at least some of your housing costs. Indeed, you could argue you have a foot on the bottom rung of the housing ladder.

So to truly answer the question of whether it’s cheaper to build or buy a house, you’ll need to do a lot of homework.

In fact, you may not be entirely sure until you’ve found the plot you want, obtained estimates from contractors, and compared those costs to similar existing homes in the neighborhood.

Verify your home loan eligibility. Start here (Aug 29th, 2022)

Buying a new home vs. existing home

There’s one more option. And that’s to buy a new-build home, which is a new house that was only just constructed, but that you didn’t have built for yourself. There are benefits and drawbacks to this strategy as well.

Back in 2017, Trulia estimated that homebuyers paid a premium of about 28% when they bought a new home.

So it might cost you $512,000 to buy a new home that’s comparable with a $400,000 existing home ($400,000 + 28% = $512,000).

Trulia’s article had the headline, “What You’ll Pay for That New Home Smell.” And it’s true that the smell is nice, as is the prestige that a newer home brings. Better yet, you’ll probably have the latest of everything: technologies, finishes, construction techniques, and more.

Home warranties and other savings

There are also solid financial perks to owning a brand new home. For example, you’re way less likely to face unexpected upgrades and expensive renovations.

If you do, those repairs may be covered by the builder’s warranty. NOLO, a legal website, suggests such warranties commonly provide the following protections:

- One year on labor and materials

- Two years on mechanical defects (air conditioning, electrical, heating and ventilation systems, and plumbing)

- Ten years on structural defects in the home

Of course, if you’re using general contractors to build your own new home, you’ll have to negotiate warranties with them.

So you stand to make savings on home repairs by buying new. But there can be other financial benefits. You’ll typically have better insulation than an older home provides and may have more energy-efficient systems and appliances. And all that should deliver lower utility bills, besides helping you do your bit for the planet.

True, it’s hard to assign dollar values to your likely savings. But you should take them into account when deciding on whether or not it’s more expensive to buy or build your own home.

Is it cheaper to buy or build a house in today’s market?

So far, we’ve explored the general principles in the buy-versus-build contest. But what differences do the current economy and property market make?

This article was written as global forces such as supply-chain issues and inflation were pushing construction costs sky-high, when making predictions was even more difficult than usual. But here are some factors that might swing your take on whether it is better to build or buy a house in 2022 and beyond:

- Inventory shortage: There are just too few homes available to satisfy demand. That’s unlikely to change for years because the only way out is to build more homes. It could take years or more than a decade to build enough

- Shortage of labor to build: 2021 and 2022 were unusual years for employment. Some older Americans retired early, and record numbers of young people dropped out of employment to start their own businesses. So the construction industry had a hard time putting boots on plots and paying higher wages to attract workers

- Current material costs: The Covid-19 pandemic caused lingering supply chain issues that created shortages in many products, including construction materials. Take lumber as an example. According to the NAHB, “Extremely volatile lumber prices during the past year have caused the average price of a new single-family home to increase by more than $18,600.” Will building material prices keep falling or head higher in the near future? Only time can tell

There are challenges to consider in the existing-home market, too.

Buyer competition

Inventory shortages have caused home buyers to compete against each other, with many sellers receiving multiple offers above listing price.

In this market, cash buyers often get priority. Their offers are not contingent on financing. And they’re treated as a sure bet while those who need mortgages may be considered riskier. That often applies even if mortgage borrowers have been preapproved by their lenders.

In areas where the real estate market is especially hot, some home buyers have seen several — sometimes dozens of — offers turned down. You can’t blame many for becoming demotivated.

You may be reading this because you’re one of those, and you’re now thinking of building your own home because buying one has so far proved impossible.

That may well be a smart move. But don’t expect an easy ride. The upfront costs of construction materials could hit you hard (especially with price hikes related to the pandemic and supply chain issues).

“If you can think of anything that can go wrong, it’s gone wrong. It’s not just one thing that’s occurred, it’s a multitude of things that have occurred,” he said.

“There is nobody to blame and the builders have suffered. They’re stuck on fixed-priced contracts and you’re seeing builders go broke.

“I don’t think anybody has done well out of this, whether it’s the builder, homeowner, supplier or the contractor.”

Tips for dealing with builders:

Careful examination of any contract with a builder is essential, so never feel pressured to sign on the spot. Take the contract home to review. Most building contracts these days tend to be plain English, but it will always be in your best interests to have a professional review any legal document.

If you establish that your contract is in good shape, with the risk of any blowout in costs resting on the builder, there is another important step to consider: make sure your builder is in good financial shape. This is particularly important in times when construction companies may be operating on low margins in an uncertain market. So, what can you do to protect yourself?

- Avoid contracts that require a large deposit. For example in NSW, the deposit cannot exceed 10% of the contract value. Making large payments when work has not yet been completed is a risk best avoided.

- Look at how many progress payments are required. Generally speaking, most builders can operate with 5 or 6 progress payments, depending on the size of works and other factors. If a builder is requesting greater than 10 progress payments, this may be an indication of potential cash flow issues, so tread carefully.

- Finally, go ahead and ask the builder about their financial situation, for those that avoid providing an answer, you may wish to avoid doing business with them.

If you have any questions about construction loans, don’t hesitate to reach out to one of our experienced YBR Home Loans experts to discuss your concerns!

UNIQUE FRENCH OCEAN VIEW HOME SAINT-TROPEZ • €34,500,000 5800m². Email: admin@y-realtor.com

Unique Historic Colonial 1860's Western Hotel 93 Cambridge Street, Mitchell, Qld Aust. $2,950,000

Click Here for INL News Amazon Best Seller Books

INLTV Uncensored News

INLTV is Easy To Find Hard To LeaveUNIQUE FRENCH OCEAN VIEW PROPERTY- SAINT-TROPEZ • €34,500,000 This unique private 5800m². property

UNIQUE FRENCH PROPERTY- SAINT-TROPEZ • €34,500,000As an aside, The Daniel FÉAU Private Collection: In absolute calm, in the immediate vicinity of the heart of Saint Tropez, global renovation / construction project of several houses or hamlet, for a total area of 740m² of living space on a quality plot of 5800m².

The project includes:

A house to renovate of 360m ² living space enjoying a sea view, a second house (friends or caretaker) of 100m ² to renovate also and two building permits obtained for two new villas totaling 260m2 of additional living space.

This unique rare as hens teeth property is a once in a life time opportunity to purchase a global develop project in the most sort after ocean front area in France. We can advise you architect and project manager. Extremely rare and qualitative set for huge long term capital growth.

Be quick to make your best offer before another shrewd investor out bids you.

Further Details on

UNIQUE FRENCH PROPERTY- SAINT-TROPEZ

Reference: 7951985

Area: 747 m²

Orientation: South-west

View: Unobstructed Sea

Waste water: Septic tank

Heating: Fuel oil Central Individual

SERVICES

Swimming pool, Fireplace, Intercom, Electric gate.

All enquires June Cambell

Email: admin@y-realtor.com

171 ALLAN ROAD Conway QLD 4800 $4,900,000

- Development / Land

- 32.37 ha

- 171 Allan Road, Conway QLD 4800

171 ALLAN ROAD Conway QLD 4800

CALLING On All Couples or Developers who want to Build Two Luxury Private Dream Homes on Two Ready Made Home Sites With 60 Degrees View Of The Pacific Ocean, On 80 acres of Absolute Pacific Ocean Frontage and 10,000 Acres Of Protected Rain Forrest on The Northern Boundary....

First To View This Unique Irreplaceable Property will Buy!!!

To enquire to purchase

171 ALLAN ROAD Conway QLD 4800. Email: admin@y-realtor.com

Are you a developer with a passion for creating new places and spaces? This stunning block of land sits directly on the waters edge, is brimming with endless future opportunities just waiting to be entertained. Spanning over approx. 80 beautiful acres, this block sits at the end of the street, has house pads already cut at the top of the block, plus a private driveway away from the street.

The panoramic views are absolutely prestigious from this undulating block, and it would be the perfect location for the newest addition to the Peppers Resort or ClubMed families of hotels. There is also subdivision potential with the right zoning upgrades.

Originally masterplanned as an Ecotourism Resort, with plenty of international and unique flora growing on the block. Plans available on request.

30.29 hectares - approx. 80 acres

Zoning changes subject to council approvals.

Bring your builder, town planner and some creativity, and you have yourself an incredible future business.

- Development / Land

- 32.37 ha

The real estate advice provided by Y-Realtor.com was extremely helpful in obtaining a good price for our property. We previously had real estate agents tried to convince us that we should sell our property for a lot less sale price than we finally achieved from through Y-Realtor.com ....... John and Liz Robertson

Australian house build cost jumps $94,000 in fastest rise since 1982: ABS, HIA stats reveal. Australia's typical house build cost has soared more than $94,000 in 15 months in its biggest surge since McMansions were taking over our suburbs in 1982.10 Jul 2022

Nathan Mawby, Property journalist

Updated 29 Aug 2022,

The cost of building Australian homes is rising faster than at any time since 1982. Picture: Dan Himbrechts

Shock new figures revealed in analysis by the Housing Industry Association and News Corp Australia show how the price of the new home dream has exploded since July 1970, when the average new build cost just $11,543.

The head of the Builders Collective of Australia has warned the latest increases, unlike anything he has seen in close to 50 years as a builder, could force half the nation’s builders into insolvency.

The staggering growth is also hitting the nation’s mortgage payers, with the cost of housing a key component of the inflation figures driving the Reserve Bank of Australia’s 1.5 per cent increase rate hike over the past three months.

Analysis of the Australian Bureau of Statistics’ most recent building approvals data shows the average price of a new house approved in the nation’s private sector in May was $413,436.

Remarkably, the figures also reveal the cost of building a new home actually declined for the first half of the Covid-19 pandemic to $319,259 in February, 2021.

HIA chief economist Tim Reardon said this was due to a glut of first-home buyers building smaller, cheaper homes after the federal government offered $15,000-$25,000 HomeBuilder grants before it was concluded in March, 2021.

Australia's national average home build cost from 1970 to today. Data compiled based on ABS figures.

But building approvals continued to surge as “the more people stayed at home through lockdowns, the more new homes they wanted”.

“We are looking at the fastest rate of growth in the average cost of an approved house build since 1982,” Mr Reardon said.

In Victoria, which is building more new houses than any other state, there was a $32,000+ jump in the typical house’s approved construction costs from March to April.

Mr Reardon said he believed cost increases would slow as the nation pulled back from building 150,000 new houses in the past year to a more typical 108,000 by 2024-2025, but the coming 12 months is likely to be the second fastest growth period in the past 40 year

............................

Rising cost of building materials is getting worse on a weekly basis, TDs to be told

The Irish Home Builders Association will tell TDs that the situation is getting worse on a weekly basis.

https://www.thejournal.ie/building-materials-cost-rising-5772050-May2022/

May 24th 2022,

RISING COSTS OF building materials are putting homes “further and further out of reach” of people who need them, the Irish Home Builders Association (IHBA) will tell TDs later today.

In their opening statement to the Joint Oireachtas Committee on Housing, Heritage and Local Government, Director of the IHBA James Benson will tell TDs and Senators that recent increases in material costs are not helping with the affordability of housing.

“Affordability remains challenging and recent extraordinary increases in the costs and availability of materials do not help. Supply is not meeting demand,” Benson will tell politicians.

“With mounting construction costs home builders are challenged to bring new homes to the market at a level that average income earners can afford.

“Residential material costs are going up on daily basis and putting homes further out of reach of those who so desperately need them.”

Benson will say that the situation is getting worse on a weekly basis and that if this increased cost of delivery isn’t added to the purchase price of a home, the pre-tax profit margins drop and builders will not meet the criteria to finance the development.

He will add that where this price is added to the purchase price of a home, it diminishes the ability of a consumer to secure a mortgage and “those currently ‘locked out’ of the market are further restricted”.

The group will also tell TDs and Senators that half of the cost of bringing a new house to the market is made up of so-called ‘soft costs’, including VAT, taxes, land costs and professional fees.

“These costs are often incurred over years in advance of commencement. There is potential to streamline those costs, deliver homes sooner, reduce costs and make homes more affordable,” Benson will say.

“There is a difference between construction costs and development costs and asking the new home purchaser to pay for all these soft costs is inequitable when compared to the second-hand home market.”

The Society of Chartered Surveyors Ireland (SCSI) are also set to tell the Joint Committee that the increased construction costs are due to both the current levels of inflation as well as price volatility for building materials.

Earlier this month, it was announced that the Government would be paying up to 70% of inflation-related costs on State projects, with Public Expenditure Minister Michael McGrath saying it was due to the threat of projects not being completed.

According to the SCSI, these are particularly insulation, cement, plasterboard, metals and fuel, alongside labour shortages and high demand for housing projects.

“In respect of the first half of 2022, it’s clear Russia’s invasion of Ukraine is having an impact on the price of materials previously sourced from the region especially steel and base metals while it has also led to a dramatic increase in fuel and energy costs,” the SCSI will tell TDs.

While the SCSI will say there is no single solution to the rising costs, it will require a “proactive and cohesive” response from the Government, while suggesting that local authorities are resourced to allow for faster processing times.

Labour shortage

The IHBA are also set to raise concerns about the labour shortage within the construction industry, saying that 27,000 more workers are needed within the residential construction industry to meet Government targets.

“While we are already witnessing greater numbers enter the sector across the various professions and trades, we need to continue to make the sector attractive to new entrants and remove current blockages,” Benson will say

“Work permits for those coming from outside the EU are currently taking 16 weeks, this is too long to expect someone to wait when we badly need workers,” adding that additional resources are set to be implemented within the Department of Enterprise.

The IHBA will also call for an improved trade traineeship model that would range from six to 18 months, depending on the type of work.

Australia’s typical home build has become vastly more expensive since 2021.

Buyers hoping costs will fall with demand have been warned not to wait.

“There have only been five instances of that in 50 years, and usually that fall is followed by strong growth,” he said.

Builders Collective of Australia president Phil Dwyer has been constructing houses since the 1970s and 1980s, when rising home-building costs were driven by buyers’ desires, not material prices.

“All of a sudden we had everyone wanting a McMansion rather than a three-bedroom home in the suburbs,” he said.

Significant changes to the way the industry works since then have left builders extremely exposed to rising material costs, particularly with builders’ margins plunging from around 20-25 per cent to 8-10 per cent.

National president of the Builders Collective of Australia Phil Dwyer, photographed in 2017. Picture: Jake Nowakowski.

“And when I started there was a mutual agreement that you would vary the contract because of circumstances and that was generally accepted, though not necessarily a given,” Mr Dwyer said.

With fixed-price contracts now leaving builders little wiggle room, he warned there would be a rise in particularly smaller builders going to the wall in the coming months.

“It could be up as high as 50 per cent in the next 12 months after Christmas,” he added.

More established groups with significant reserves to fall back on were more likely to survive, he said.

Mr Dwyer added he hoped he was wrong about his predictions, but said “I have never seen the cards laid out the way they are at the moment — I have never seen it this bad”.

Housing construction is expected to slow in Australian suburbs in the coming years.

Burbank Homes national general manager Louis Sultan said labour, concrete, steel and hardware remained problematic for costing.

“So the quicker you can lock in your new home contract the more certainty you will have about what your new home will cost,” Mr Sultan said.

In response to rising costs, many buyers were now prioritising upfront expenses that will save them money in the future, particularly around energy efficiency, solar panels and electric vehicle systems, plus more water and energy-efficient appliances, he added.

Any efforts by the government to stabilise imports and exports would improve supply chains for building materials, Mr Sultan said.

Housing Industry Association chief economist Tim Reardon.

Finding ways to get builders onto sites faster after a buyer had purchased a block of land could also help builders quote more accurately.

Mr Reardon said an increase in the number of stage payments, currently mandated at five for a typical house, would give builders more flexibility without any risk to customers.

Sign up to the Herald Sun Weekly Real Estate Update. Click here to get the latest Victorian property market news delivered direct to your inbox.

The house prices that are still rising: How inflation is blowing out building costs

July 19, 2022

Property prices may be falling for the established housing market, but new homes are bucking the trend and have become the canary in the coal mine, as far as inflation goes.

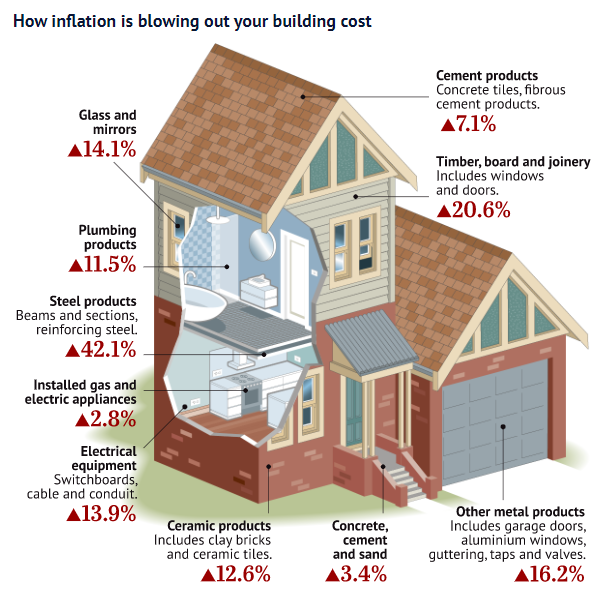

Almost every category of building materials has become more expensive. Steel products are leading the way, jumping 42.1 per cent in the year ending March 2022, Australian Bureau of Statistics figures show.

It was followed by timber, board and joinery, which jumped 20.6 per cent in the same period.

The soaring costs are a sharp turnaround and at odds with the falling prices of established housing market thanks to the sheer two-year strong demand for new homes, in the face of ongoing limits on materials and labour to build a house.

It all began when the majority of households pumped almost any spare dollar into their homes where they bunkered down once they realised they could hold on to their jobs during the pandemic and government support in the form of JobKeeper flowed through, as well as spending initiatives such as HomeBuilder.

As a result, the residential construction industry became the canary in the inflationary coal mine, according to Denita Wawn, chief executive of Master Builders Australia.

“It’s been a rollercoaster … two years ago, contracts were being terminated because everybody thought they would lose their job. All of a sudden, JobKeeper and HomeBuilder came along and people weren’t travelling, the building industry went from no work to too much work,” Wawn said.

Australians, who typically spend $55 billion a year travelling overseas, found themselves cooped up at home with cash to spare, she said.

“It had to go somewhere, so people were spending it on their homes,” Wawn said. “We were a bit of a canary in the inflationary coal mine. Inflation hit us hard 12 months ago.”

If Australians did not sign up to build a new home, they at least spent money improving it in some way, as shown by record building approvals and renovation spend.

The Housing Industry Association chief economist Tim Reardon said the rise of construction costs was twofold.

First was the sheer pickup in the demand for houses in speed and volume, Reardon said, then came the constraints on supply and labour that failed to meet that unprecedented demand, which was compounded by the fact most other developed economies had the same housing boom at the same time.

Before the pandemic, the construction of freestanding houses was slowing, with about 105,000 being built, the Association’s figures show.

By the end of 2021, that had increased by almost 50 per cent. That has now jumped to 80 per cent more homes under construction than pre-COVID, Reardon said.

“We have seen a 19 per cent increase in the value of the average home approved in Australia over the past 12 months to May,” he said.

“It’s been very difficult for builders to price the construction of a home … given the rapid increase in prices and builders typically bear that risk, which has been a challenging time for builders and businesses.”

At one point, when Canberra went into a snap two-week lockdown, it took just five days for roofing battens to run out on the entire east coast, as the city was the only location the product was produced, Reardon said.

“It’s those additional shocks that disrupted the efficient operations of the industry and have added costs throughout the supply chain. All those factors compound through, and those costs are borne through by those building new homes.”

Brick manufacturing locally has increased, but ramping up production takes time to commission new plants and train new staff, he said.

Home building in the next 12 months will remain at capacity, but the number of approvals will slow down as rising rates and the construction costs start to bite households, Reardon said.

“The end outcome is the increased cost of new homes will slow the demand for new homes, compounding that is the increase in the cash rate,” he said.

Jon Stoddart, managing director of Stoddart group, Australia’s leading supplier and installer of products to the residential building industry, said the sector has been impacted at every step of the building process, compounding inflationary pressures.

“First there was the home stimulus grant. We sold a bucketload of houses then freight got dearer, then worldwide timber took off. To top that off, a lot of the timber that comes out of Russia was banned, that limited that supply,” Stoddart said, adding that they resorted to using steel frames as an alternative.

But during recent floods train lines used to transport heavy steel loads were destroyed, disrupting the alternative supply chain once again, as well as a labour shortage as insurance companies pay top dollar to complete urgent flood claim works, Stoddart said.

https://www.macrobusiness.com.au/2022/07/australias-home-builders-crushed-by-escalating-costs/

Australia’s home builders crushed by escalating costs

By Unconventional Economist in Australian Economy, Australian Property

at 12:03 am on July 28, 2022 | 64 comments

Australia’s home building industry is in crisis with dozens of firms going under in 2022.

The primary cause is the escalation of input costs across the construction process, as illustrated in the below graphic from Fairfax:

Extreme inflation in building costs.

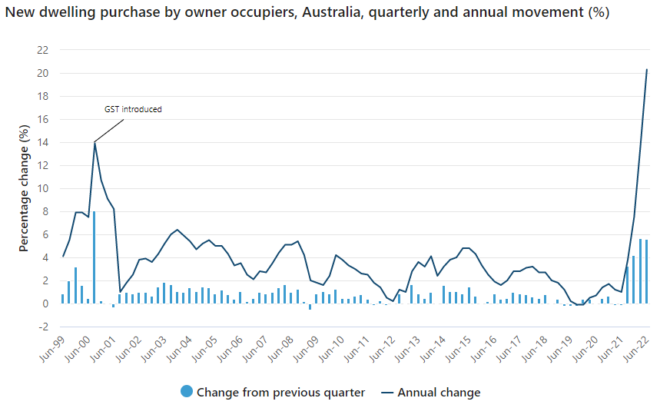

Yesterday’s June quarter Consumer Price Index (CPI) from the Australian Bureau of Statistics (ABS) sent another dagger through the heart of the building industry. It revealed that “new dwelling prices recorded their largest annual rise since the series commenced in the June 1999 quarter”, reflecting “high levels of building construction activity combined with ongoing shortages of materials and labour”:

New dwelling prices soar on rapid cost inflation.

New dwelling prices soared 20.3% in the 2021-22 financial year, easily eclipsing the 13.9% increase when the GST was introduced in 2000.

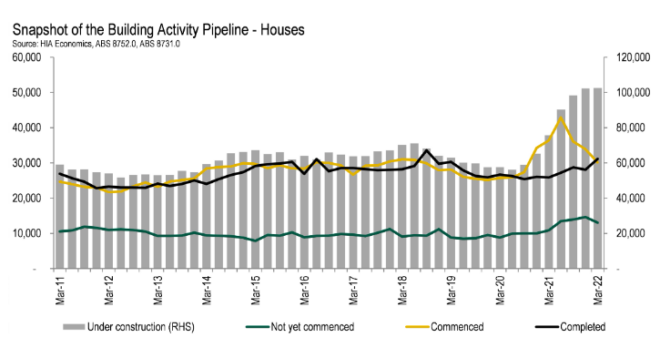

Despite a record number of homes under construction (see below chart), builders are dropping like flies because the cost of construction has in many cases risen above their fixed price contracts.

Record number of homes under construction.

Basically, Australia’s home building industry is caught in a “loss-making boom”, where they are busier than ever, but losing money on every home built.

The situation has important ramifications for both the housing market and economy.

The construction industry employs around 9% of Australians, with the majority of these working in home building. Therefore, any sharp downturn in dwelling construction will necessarily have a major impact on the jobs market.

Australia’s rental market is also the tightest on record just as the federal government is about to open the immigration floodgates. So, if enough builders are driven out of the industry, it will reduce future housing supply when it is needed most, worsening affordability.

Sadly, there are no easy solutions. Many more builders will go to the wall before the supply pressures ease.

Unique Historic Colonial 1860's Western Hotel 93 Cambridge Street, Mitchell, Qld Aust. $2,950,000

Unique Historic Colonial 1860's Western Hotel 93 Cambridge Street, Mitchell, Qld Aust. $2,950,000

Unique Historic Colonial 1860's Western Hotel 93 Cambridge Street, Mitchell, Qld Aust. $2,950,000

Puts me on the street': Americans forced out of homes as rents skyrocket

521

Historic 1860's Western Hotel 93 Cambridge Street, Mitchell, Queensland, Australia is on the market for an asking price of $2,950,000.

If you are Running a holiday sale or weekly special? Definitely promote it here to get customers excited about getting a sweet deal. Email us at: admin@y-realtor.com for a free complimentary ad.

Buy or build a house: What’s cheaper? 2022 Cost comparison

The Mortgage Reports EditorJuly 19, 2022 - 9 min read

Should you build or buy a home?

With home price inflation continuing its upward path, many would-be buyers are considering alternatives — like building their own house from scratch rather than buying an existing one.

But that begs the question, is it cheaper to build or buy a house?

If you compare average build prices to average purchase prices, building your own home is generally more expensive. But there are so many variables that this is far from certain in every case.

Wondering whether to build or buy in 2022? Here’s what you should know.

Verify your home loan eligibility. Start here (Aug 29th, 2022)

In this article (Skip to...)

Is it cheaper to build or buy a house?

As a rule of thumb, it’s cheaper to buy a house than to build one. Building a new home costs $34,000 more, on average, than purchasing an existing home.

The median cost of new construction was $449,000 in May 2022. Comparatively, the median cost to buy an existing home was $414,200, according to the most recent data available from the National Association of Home Builders (NAHB) and the U.S. Census Bureau.

- Average cost to build a house: $449,000

- Average cost to buy a house: $414,200

The cost of building a new house includes buying a plot, excavations, permits, inspections, and other associated costs.

However, the data reveals a significant drop in costs for those who already have a lot on which to build. A separate study from the NAHB, dating back to 2019, ballparks the purchase price for a plot to be 18.5% of the total costs for new construction. This bumps down the cost of building a home to an estimated $365,935 for those who already own a lot.

So, which is the right choice? That depends on many factors — like your needs, location, timeline, local home inventory, and the availability and prices of materials and labor.

Let’s dig into these factors a little further to help you weigh the costs and benefits of building versus buying.

Check your home buying options. Start here (Aug 29th, 2022)

Financing a new construction home

Yet another variable is your financing plan. Some people use a mortgage to buy the land and then use savings or a construction loan to fund the project.

But then, when the work is finished, you’ll usually have to refinance the mortgage to repay the bank or replenish your savings. And that means two sets of closing costs: One for the original land purchase loan and another for the refinance.

Meanwhile, construction loans typically come with higher interest rates than standard mortgages. Additionally, there are strict rules about the timeline for construction and disbursement of funds.

An alternative is to get a construction-to-permanent loan. With one of these, you borrow using a single loan to buy the land and build the home. Money is released as you reach preset construction milestones.

For more information, read: Financial steps to building a house: The complete guide

Average cost to buy a house

In May 2022, the median home sales price for an existing house was $414,200 according to the NAHB and U.S. Census Bureau.

But, just as construction costs vary by state, so do home prices. Indeed, there can be enormous differences within states by city, county, and neighborhood.

For example, buy a home in Ilion, New York, and you can expect housing costs that are roughly 800% less than the statewide average. But purchase one in Chelsea, NYC, and you can expect to pay dearly. The median sale price there in April 2022 was an astronomical $2 million, according to Realtor.com.

Home price inflation

There’s yet another component in your decision-making process. How quickly are home prices rising where you want to buy or build?

In June 2022, CoreLogic reported that home sales prices nationwide, “increased year-over-year by 20.9% in April 2022 compared with April 2021.” That’s an annualized figure, meaning home prices in April 2022 were 20.9% higher than they were 12 months earlier. Furthermore, no states reported an annual decline in home values.

Again, that’s a nationwide average. If you’re a first-time buyer, home prices where you want to live may well have risen more gently. But it’s just as likely they’ll have shot up even more sharply.

For example, if you wanted to buy in Arizona, Florida, or Tennessee, CoreLogic says prices in all three states rocketed by more than 27% over those 12 months. That might influence your decision over whether to build or buy your home.

Consider your timeline

Should you divert some of your down payment savings into buying a plot now? You could then sit on it until you can afford to begin construction on your dream home. That way, you’d have control over at least some of your housing costs. Indeed, you could argue you have a foot on the bottom rung of the housing ladder.

So to truly answer the question of whether it’s cheaper to build or buy a house, you’ll need to do a lot of homework.

In fact, you may not be entirely sure until you’ve found the plot you want, obtained estimates from contractors, and compared those costs to similar existing homes in the neighborhood.

Verify your home loan eligibility. Start here (Aug 29th, 2022)

Buying a new home vs. existing home

There’s one more option. And that’s to buy a new-build home, which is a new house that was only just constructed, but that you didn’t have built for yourself. There are benefits and drawbacks to this strategy as well.

Back in 2017, Trulia estimated that homebuyers paid a premium of about 28% when they bought a new home.

So it might cost you $512,000 to buy a new home that’s comparable with a $400,000 existing home ($400,000 + 28% = $512,000).

Trulia’s article had the headline, “What You’ll Pay for That New Home Smell.” And it’s true that the smell is nice, as is the prestige that a newer home brings. Better yet, you’ll probably have the latest of everything: technologies, finishes, construction techniques, and more.

Home warranties and other savings

There are also solid financial perks to owning a brand new home. For example, you’re way less likely to face unexpected upgrades and expensive renovations.

If you do, those repairs may be covered by the builder’s warranty. NOLO, a legal website, suggests such warranties commonly provide the following protections:

- One year on labor and materials

- Two years on mechanical defects (air conditioning, electrical, heating and ventilation systems, and plumbing)

- Ten years on structural defects in the home

Of course, if you’re using general contractors to build your own new home, you’ll have to negotiate warranties with them.

So you stand to make savings on home repairs by buying new. But there can be other financial benefits. You’ll typically have better insulation than an older home provides and may have more energy-efficient systems and appliances. And all that should deliver lower utility bills, besides helping you do your bit for the planet.

True, it’s hard to assign dollar values to your likely savings. But you should take them into account when deciding on whether or not it’s more expensive to buy or build your own home.

Rising home values for existing homes

Rising home prices are great for existing homeowners. In June 2022, CoreLogic reported an average annual equity gain of $64,000 per borrower between the first quarters of 2022 and 2021. That’s a 32% increase from the previous year.

In other words, the average homeowner’s wealth jumped by $64,000 in a single year without them lifting a finger. What’s not to like?

Well, a lot, if you’re a first-time buyer or someone who sold their home and can’t find a new one. Because your buying power is reducing all the time — and quickly.

The good news for such buyers is that many expect home price increases to slow dramatically in 2022. So while home values should keep rising, if the experts are right, the worst of skyrocketing prices could be behind us.

Bottom line: Building vs buying a house

So, is it better to build or buy a house? You’re now much better informed on that topic than you were when you started this article. But you probably won’t be much closer to making a decision.

That’s because of all those homeownership variables we mentioned earlier, including:

- Construction costs where you wish to build, including possible labor shortages and price hikes for materials

- Home price trends in the area where you want to live

- The size and specifications of the home you want

- Whether you have the skills and time to do some of the work yourself

- Whether you’re prepared to live in temporary accommodation while construction is completed

- The type of mortgage you choose

Unfortunately, there’s no definitive answer to the original question: Is it cheaper to build or buy a house? The only way you can find out is by running the figures for your own unique situation.

If you know a local real estate agent and contractor, you may be able to model the cost of building for both a theoretical purchase and construction project, then compare them to see which is more affordable.

But, otherwise, you probably need to find a plot and get contractors’ quotes. Then you can compare costs of the home you might build with those for purchasing something similar. Only with those can you make your final choice.

Cons of buying new build

- Space – Some developers pack a lot of properties onto a site in order to maximise their profits. This can mean a new-build home is less spacious than an older property. We know from experience this can particularly affect storage space and the size of the rooms. Check that your furniture fits and that your car will get into the garage.

- New home premium – A lot of the benefits of buying a new-build disappear on the day you buy it and it is no longer “brand new”. This means a one-year-old property may fall in value as buyers look at the new-builds popping up in the development across the road instead. Our advice is, if you are buying a new-build, plan to live in it for the longer term.

- Estate management charges – Many new build estates are not being adopted by the local council and are being managed privately by management companies. This means that the new build owner has to pay for the maintenance of the playground and shared spaces. These costs can escalate and owners find that they have no right to challenge the charge or change the management company. This is a growing issue for owners on new build estates and can be a real con to buying new build.

- Leasehold – Flats are sold as leasehold rather than freehold. This means you will need to pay annual service and maintenance charges as well as ground rent. Make sure your conveyancer explains costs, charges and restrictions set out in the contract and include them in your cost of owning a home. Find out more before you start looking round showrooms with our guide to Leasehold Charges. The length of the lease is also critical – it should be at least 90 – 120 years and preferably 999 years.

- Complicated legal work – New build conveyancing can be more complex then buying an older property. We also often hear from our users that a developer insisted they used their recommended conveyancer in order to purchase a new-build. This should be avoided at all costs. A good solicitor with experience of new build conveyancing but not partnered with the developer will ensure that the contract is in your favour, that your deposit is fully protected and that there is a ‘long-stop’ completion date for the property to be finished by. The developers solicitor and sales team will exert huge pressure on you to complete, while a conveyancing solicitor chosen independently is less likely to bend under pressure.

- Quality and Snags – New builds often get a bad press with stories of poor quality making the headlines. Even with the best new build home, you can still expect snags like doors getting stuck on new carpets or a loose tile. Whether it’s a significant structural issue or a series of small annoying snags, be prepared to have a snagging survey as soon as the developer will let you on site. This way a professional who knows what they are looking for will be able to reassure you everything is as it should be. They will also liaise with the builder to get everything sorted out.

- Delays – New builds don’t always run to plan and it isn’t unusual for the move-in date on a new build property to be delayed. This could just be an inconvenience, but if it goes on it can cause added stress and add to your costs. We hear from people daily struggling with unexpected rent and storage costs, having moved in to alternative accommodation awaiting their new builds completion. Too long a wait can also affect mortgage offers.

Looking for a conveyancing solicitor to oversee the purchase of your new build home? Compare conveyancing quotes

One Billion Dollar Rinehart-Senex Energy Gas Expansion & Film Projects In and Near Mitchell, Qld

Unique Historic Colonial 1860's Western Hotel 93 Cambridge Street, Mitchell, Qld Aust. $2,950,000

One Billion Dollar Rinehart-Senex Energy Gas Expansion & Film Projects In and Near Mitchell, Qld

Why so many Aussies are swapping the city for the country | 60 Minutes Australia

Western Hotel 93 Cambridge Street, Mitchell, Queensland, Australia $2,950,000 asking price. Gas producer Senex, which is jointly owned by South Korea's steel giant Posco and Australian billionaire Gina Rinehart, has planned a more than $1 billion expansion to its Queensland gasfields to its Atlas and Roma North, near the town of Mitchell, Queensland. The bulk of the extra gas fuel apparently to be earmarked for domestic use in Australia. This $1 billion investment would triple Senex's annual output of about 20PJ of gas in 2021 to 60PJ. Two thirds of the planned investment would be spent in the next two years, which will create a large number of jobs and create substantial long term economic growth in the town of Mitchell, and the Maranoa Region that surrounds the town of Mitchell, Queensland, which Mitchell services. See: www.thegardian.com, www.bloomberg.com, www.afr.com, www.ginarinehart.com,www.hancockpropsecting.com.au, www.thewest.com.au, www.finance.yahoo.com, www.theaustralian.com.au, www.abc.com.au, www.skynews.com.au, www.ppo.com.au, www.latestly.com, www.energynewsbulletin.net, www.crikey.com.au, www.heraldsun.com.au

The Western Hotel at 93-95 Cambridge Street, Mitchell, Queensland, Australia, 4465 has been selected as a base and prop to make various feature films, TV and Internet Shows and the development of websites by the tenant Yahoo Real Estate Pty Ltd and Yahoo Real Estate Pty Ltd's film and investment partners

https://www.4321property.com/australia/ad940009/?redirecttoad=1&adsensesanitize=off

To enquire to purchase 93 Cambridge Street, Mitchell, Queensland, Australia

Email: admin@y-realtor.com-

The Western Hotel 93-95 Cambridge Street, Mitchell, Queensland Australia, 4465

The Western Hotel 93-95 Cambridge Street, Mitchell, Queensland Australia, 4465

Average cost to build a house

NAHB put the average cost to build a house at $449,000 in May of 2022. That’s including the cost to buy a plot of land.

With the land purchase included, there’s an 8% gap between the average price of building and buying. And building could end up being substantially more expensive depending on your location, construction plans, and the cost of materials and labor.

What impacts the cost of building a home

First is the cost of construction. This can vary a lot not only by the home builder, but also depending on the cost of materials and when you want to build.

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot or much more if you want the best of everything.

If you have the time and skills to do some of the construction work yourself, that might bring big savings. Just don’t try to do work that’s beyond your capabilities. There will be independent inspections and the home must be mortgageable to have a sensible resale value.

Then there’s the location.

HomeAdvisor reports that it can cost more than twice as much to build in Alaska as in Kansas. And between those two extremes, range the costs in all the other states.

Other building costs to consider

Other variables in the building process include:

- Site costs: Home builders have multiple site fees, including those for building permits, water and sewage inspections, and architectural and engineering plans, to name a few

- Foundation: A new home with a basement will increase the overall costs. But even without one, you’ll still pay for excavation, foundation, concrete, and retaining walls

- Framing and exterior finishes: Not only do these costs vary depending on the square footage of the home and its floor plan, but you’ll also need to figure in the price for building materials and labor costs (such as your general contractor and any subcontractors)

- Major home systems: These include plumbing, electrical, and HVAC. Again, labor costs for plumbers and electricians also apply

- Interior finishes: Don’t forget your custom home’s flooring, drywall, countertops, appliances, and other amenities

- Plot: Landscaping, outdoor structures, decks, driveways, and cleanup costs

You can build a basic home for about $150 per square foot of living space. But it’s easy to spend $500 per square foot if you want the best of everything.

And, no doubt, you could easily bust that top figure if you choose to import acres of Calacatta Carrara marble from Italy for your 5,000-square-foot home.

Plan for overruns

Of course, some construction projects sail through on time and on budget. But it’s very common for both to overrun. So you should build in a 5% or 10% contingency to take care of unexpected building costs. And more if you’re the sort of person who’s easily tempted to overspend when confronted with a range of choices.

Is it cheaper to buy or build a house in today’s market?

So far, we’ve explored the general principles in the buy-versus-build contest. But what differences do the current economy and property market make?