About Us

Property Stamp Duty Cost in Queensland Australia

Property Stamp Duty Cost in Queensland Australia

Property Stamp Duty Cost in Queensland Australia

Your ultimate guide to stamp duty in Queensland

https://www.realestate.com.au/home-loans/guides/how-much-is-stamp-duty-in-queensland $75,000 to $540,000 - $1,050 plus $3.50 for each $100, or part of $100, over $75,000

https://www.realestate.com.au/home-loans/guides/how-much-is-stamp-duty-in-queensland $75,000 to $540,000 - $1,050 plus $3.50 for each $100, or part of $100, over $75,000

What is stamp duty?

As with other states and territories, if you’re buying a residential property in Queensland, yo

Your ultimate guide to stamp duty in Queensland

https://www.realestate.com.au/home-loans/guides/how-much-is-stamp-duty-in-queensland $75,000 to $540,000 - $1,050 plus $3.50 for each $100, or part of $100, over $75,000

What is stamp duty?

As with other states and territories, if you’re buying a residential property in Queensland, you’ll need to pay stamp duty. However, unlike some parts of the country, concessions aren’t limited to first-home buyers. Those planning to occupy their home, rather than invest, may also be eligible for a discount.

In Queensland, transfer duty, sometimes called stamp duty, is a tax charged by the state government whenever a property is sold or transferred to a new owner.

It’s paid by the person who buys, or is given, a property, not the seller.

How much is stamp duty in Queensland

The cost of stamp duty depends on the value of the property. It’s calculated on a sliding scale, so the more expensive the property, the more stamp duty you’ll pay.

However, what you plan to do with the property also affects the amount you’ll pay.

The state government has a general rate of stamp duty, which applies to investment property purchases. If you plan to live in the property, a home concession will apply. First-home buyers are also eligible for discounts.

Calculate stamp duty for Queensland

Calculate the stamp duty you may have to pay on your property

https://www.realestate.com.au/home-loans/guides/how-much-is-stamp-duty-in-queensland

General rate of stamp duty in Queensland

For those buying an investment property, the following standard transfer duty rates apply:

Purchase price/value Transfer duty rate Not more than $5,000 Nil More than $5,000 up to $75,000 $1.50 for each $100, or part of $100, over $5,000 $75,000 to $540,000 $1,050 plus $3.50 for each $100, or part of $100, over $75,000 $540,000 to $1,000,000 $17,325 plus $4.50 for each $100, or part of $100, over $540,000 More than $1,000,000 $38,025 plus $5.75 for each $100, or part of $100, over $1,000,000

For more information visit the Queensland government’s website.

Home concession

If you’re purchasing as an owner occupier you’re entitled to a discount, as long as you meet certain requirements. Eligible buyers can claim the home concession regardless of whether or not it’s their first home.

The home concession rate applies to the first $350,000 of value of the residence, and the general transfer duty rates then apply to the balance. If eligible, buyers could save up to $7,175.

The home concession rate is set out below.

Purchase price/value Home concession rate Not more than $350,000 $1.00 for each $100 or part of $100 More than $350,000 to $540,000 $3,500 + $3.50 for every $100, or part of $100, over $350,000 $540,000 to $1,000,000 $10,150 + $4.50 for every $100, or part of $100, over $540,000 More than $1,000,000 $30,850 + $5.75 for every $100, or part of $100, over $1,000,000

Eligibility for Queensland’s home concession stamp duty discount

To be eligible for the home concession:

- You must live in the property as your principal place of residence within one year of settlement

- You must not sell or lease any part of the property before you move in.

If you sell or lease the property within one year, a partial concession may apply.

To find out more about the home concession on stamp duty visit the Queensland government’s website.

First home concession

First-home buyers can receive a further discount – on top of the home concession rate – on properties valued under $550,000.

It’s calculated by deducting the first home concession amount (set out in the table below) from the home concession rate.

Purchase price/value First home concession Up to $504,999.99 $8,750 $505,000 to $509,999.99 $7,875 $510,000 to $514,999.99 $7,000 $515,000 to $519,999.99 $6,125 $520,000 to $524,999.99 $5,250 $525,000 to $529,999.99 $4,375 $530,000 to $534,999.99 $3,500 $535,000 to $539,999.99 $2,625 $540,000 to $544,999.99 $1,750 $545,000 to $549,999.99 $875 $550,000 or more Nil

First home concession eligibility

You are eligible for the first home concession if you meet the following criteria:

- You’ve never claimed the first home or first home vacant land concessions

- You’ve never owned a residence in Australia or overseas

- You must move into the property within a year of settlement

- You must be over 18 (although you can apply to have this waived)

- You must not sell or lease the property before you move in.

If you sell or lease the property within one year, a partial concession may apply.

First home vacant land concession

First-home buyers buying vacant land to build their home can claim the first home vacant land concession.

It applies to land valued at less than $400,000 and is calculated by subtracting the concession amount (set out in the table below) from the standard transfer duty rate.

No duty is payable on land valued at less than $250,000, while land worth more than $400,000 will receive no concession.

Dutiable value Concession (deduct this amount from the transfer duty rate) Not more than $250,000 100% of transfer duty More than $250,000 to $259,999.99 $7,175 $260,000 to $269,999.99 $6,700 $270,000 to $279,999.99 $6,225 $280,000 to $289,999.99 $5,750 $290,000 to $299,999.99 $5,275 $300,000 to $309,999.99 $4,800 $310,000 to $319,999.99 $4,325 $320,000 to $329,999.99 $3,850 $330,000 to $339,999.99 $3,375 $340,000 to $349,999.99 $2,900 $350,000 to $359,999.99 $2,425 $360,000 to $369,999.99 $1,950 $370,000 to $379,999.99 $1,475 $380,000 to $389,999.99 $1,000 $390,000 to $399,999.99 $525 $400,000 or more No concession

First home vacant land concession eligibility

To be eligible for a first home vacant land concession:

- You’ve never claimed the first home or first home vacant land concessions

- You’ve never owned a residence in Australia or overseas

- You must build your first home and move in within two years of settlement

- You can only build one home on the land

- You must be over 18 (although you can apply to have this waived)

- You must not sell or lease the property before you move in.

If you sell or lease the property within one year, a partial concession may apply.

To find out more visit the Queensland government website.

Foreign buyers and stamp duty

Buyers who aren’t Australian citizens or permanent residents can still qualify for concessions, however, they must also pay an extra duty.

REIA faces tough sell in calling for end to stamp duty

The country's peak real estate industry body has called for the abolition of stamp duty but faces a tough task convincing the revenue-dependent states to relinquish one of their main sources of income.

By Craig Francis | 6-9-2022 | Tax

https://www.apimagazine.com.au/news/article/reia-faces-tough-sell-in-calling-for-end-to-stamp-duty

The property industry’s peak body has launched a campaign to abolish a property transaction tax that now accounts for between 24 and 40 per cent of the various state governments’ revenues.

The Real Estate Institute of Australia (REIA) has stamp duty in its crosshairs as it targets the tax it says burdens first-home buyers with an additional four years of saving.

It promises to be a difficult sell to the states, whose reliance on the tax has only increased over the years while state governments show few signs of surrendering the keys to the vault.

The new national and multi-year campaign is aimed at phasing out stamp duty, which the REIA said was contributing to property supply in Australia being critically low and impacting housing and rental affordability in every state and territory.

Most commentators agreed it was a flawed tax, but as Peter White, Managing Director of the Finance Brokers Association of Australia, told API Magazine that getting rid of the tax altogether may be a utopian dream.

“The states are reliant on the revenue, so while the REIA’s campaign is a noble cause, it’s going to be a tough sell to the states, some of whom have said they’re not considering changes and others are actually raising stamp duty,” Mr White said.

'Inefficient, unfair'

REIA President, Hayden Groves, argued that as Australia moves through the current economic and real estate cycle, there is no area of reform that will have greater benefits than the phase out of stamp duty.

“With cost-of-living pressures mounting, stamp duty remains a major hurdle to first-home buyers, those wanting to move around the country or invest in much-needed rental supply.

“At a time when housing supply presents such an immense challenge, the removal of stamp duty could increase sales and rental listings by up to 50 per cent within existing housing stock.”

Mr Groves said that the removal of stamp duty, which was promised and not delivered with the introduction of a goods and services tax (GST) in 2000, would kickstart the economy, improve affordability and supply, and open opportunities for all Australians.

“There is almost universal agreement that stamp duty is an inefficient, unfair tax that stifles labour mobility and penalises those seeking to move to areas where better employment, educational or lifestyle opportunities exist.

“First-home buyers seeking to buy established homes are forced to delay buying decisions to save for stamp duty.

“Stamp duty adds about 4 per cent to the median house price of a home and adds on average $30,000 to the typical property purchased in Australia.

“Both directly and indirectly, stamp duty is contributing to property supply in Australia being critically low and impacting housing and rental affordability in every state and territory.”

New South Wales has shuffled the deckchairs around and the end result is probably neutral.

- Peter White, Managing Director, Finance Brokers Association of Australia

Mr Groves said stamp duty reform would require the will and collaboration of many across Australia’s Federation, and Axe the Tax aims to start a proper conversation on a national level.

Stamp duties as a percentage of average earnings have jumped over the past nine years to 34.3 per cent from 25.1 per cent.

The property downturn, however, is set to slash $7 billion from stamp tax revenue this year across NSW, Victoria and Queensland.

Revenue NSW figures show there were over 19,000 transactions in July, from which the NSW Government collected more than $981 million in stamp duty.

Land tax alternative

Stamp duty reform has unquestionably been on the radar of various state governments.

The latest NSW Government Budget included a new policy to offer first-home buyers the choice to pay a one-off lump sum tax, or stamp duty, or an annual land tax when purchasing homes under a certain value.

To recoup some of this lost revenue, the NSW Government will introduce an annual land tax payment. This tax will be similar to local government rates. For example, instead of paying a one-off lump sum you end up paying it each year, indefinitely, while you own that property.

The negative effect of this policy shift is that over the time that people own the home they could end up paying more.

However, the benefit is that it makes it easier for people to get into the property market quicker.

Arun Maharaj, CEO, Hashching

“New South Wales has shuffled the deckchairs around and the end result is probably neutral, although it does have some cash flow benefits in that it allows people to pay off the debt annually instead of in a lump sum, and it makes the (NSW) government look like they’re doing something,” Mr White said.

Queensland still rakes in stamp duty but has also attracted the ire of property owners around the country by expanding their land tax so that it now has national reach.

Digital loan platform Hashching CEO Arun Maharaj told API Magazine that stamp duty is a formidable barrier to people transacting on housing.

“The alternative is a land tax, which turns the lump sum into a recurring payment,” he said.

“We’re generally in favour of this, as long as the land tax remains a predictable value that buyers can easily factor into the monthly cost of their purchase alongside the mortgage.

“Convincing the public of this hinges entirely on how the tax is communicated, and the guarantees that can be put in place that a land tax will not become an issue for them later in life.”

For more on their position, the REIA has launched a new website and policy paper, The Case for Change: Stamp Duty Phase Out.

As well as enjoying a career as an international news journalist and editor with major international news organisations such as CNN (London and Hong Kong), Financial Times (UK), South China Morning …

stamp duty, REIA, Finance Brokers Association of Australia, Hayden Groves, Peter White, tax, taxation, Property Taxation, NSW, reform, state revenue, first-home buyers, Rental Shortage, affordability, Housing Supply, saving, NSW Government, Queensland Government, Hashching, Arun Maharaj, land tax, Queensland land tax, State Government

Subscribe to property

investor updates

Get the latest property investment news

delivered free to your inbox each week.

Featured Articles

Interest rates on an all-night bender while prop… 7-9-2022 | Finance

Interest rates on an all-night bender while prop… 7-9-2022 | Finance  Another interest rate double hike from aggressiv… 6-9-2022 | Finance

Another interest rate double hike from aggressiv… 6-9-2022 | Finance  Geelong Cats fan on clawing through building ind… 5-9-2022 | Expert In Focus

Geelong Cats fan on clawing through building ind… 5-9-2022 | Expert In Focus  Is this just the start of bigger price falls for… 3-9-2022 | Residential

Is this just the start of bigger price falls for… 3-9-2022 | Residential  As one Sydney construction mega project ends, an… 2-9-2022 | Development

As one Sydney construction mega project ends, an… 2-9-2022 | Development

Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance

Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance  Another interest rate double hike from aggressive RBA 6-9-2022 | Finance

Another interest rate double hike from aggressive RBA 6-9-2022 | Finance

A guide to Queensland's far-reaching new land tax

National expansion of Queensland's land tax will add a whole new layer of complexity, and potentially expenses, for any investor with property in that state but this in-depth overview from Investor Partner Group explains everything a property owner needs to know.

By Sponsored Content | 2-9-2022

https://www.apimagazine.com.au/news/article/a-guide-to-queenslands-far-reaching-new-land-tax

For anyone in Australia who owns property in Queensland, changes to that state’s land lax regime have major implications for investors and land owners.

Significant changes to the calculation of Queensland land tax liability were given the green light when the Revenue Legislation Amendment Act (Qld) 2022 was assented to on 30 June 2022.

Changes to the Land Tax Act 2010 (Qld), which will impact Queensland landowners from 30 June 2023, mean assessment of Queensland land tax liability will take into account the value of interstate landholdings.

This will mean an increase in land tax liability for anyone who owns land in Queensland as well as non-exempt property in another state or territory.

The current position

The current position (which will remain in effect for the 2022/23 financial year) is that land tax liability is determined by reference to the taxable value of the land owned in Queensland as at midnight on 30 June each year, with different thresholds and rates applied to individuals, corporations, trustees and absentees and exemptions for certain classes of landholdings.

The new land tax system

From 30 June 2023, land tax will be imposed based on the Queensland proportion of the total value of the Australian land owned by the landholder.

The total value of Australian land includes:

- the taxable value of Queensland land

- the statutory value of interstate land, being the relevant valuations applied under the relevant state and territory legislation.

The existing land tax exemptions (including primary place of residence and primary production) will remain in place under the amended legislation. Note also that the increased tax liability in Queensland does not impact on any taxes payable in other states and territories.

Working out land tax: an example

To illustrate the increase, Investor Partner Group has considered the position for an individual who owns one property in Queensland with a taxable value of $745,000 and one property in New South Wales with a statutory value of $1 million.

Under the current arrangement, the individual will pay $1,950.00 in land tax this financial year in Queensland for the Queensland property. This liability is calculated at the second tier as set out in Schedule 1 of the Act ($500 plus one cent for each $1 more than $600,000, up to $999,999).

Using the same example in the 2023/2024 financial year utilising the new system, the same individual will pay $7,169.29 in land tax (an increase of more than $5,200).

The new calculation is done in two steps:

- firstly, by applying the relevant general rate for an individual to the total value of all Australian land owned by the landholder to reach a gross rate (in this case the applicable rate being $4,500 plus $1.65 for each $1 more than $1,000,000, which for landholdings of $1,745,000 across the country amounts to $16,792.50)

- secondly, by applying this gross rate to the Queensland proportion of the total Australian land value, i.e., the tax liability = $16,792.50 x ($745,000 / $1,745,000) = $7,169.29

Notification obligations

To assist the Queensland Revenue Office in determining other Australian landholdings and the statutory value of those landholdings, amendments to the Act require Queensland landholders to provide further details by way of notice in an approved form (including property description, statutory value and interest), generally by 31 October each year or, if a Queensland assessment notice is issued before 31 October, within 30 days of receiving the assessment. Failure to comply with notification obligations will be an offence.

Practical implications

As the full force of the changes will not be felt until 2023, Moxin Reza, General Manager, Investor Partner Group, said it is difficult to say whether the amendments to the Land Tax Act 2010 (Qld) will impact on investment habits or holdings in Queensland.

However, we consider it is likely the increase in land tax will be felt by commercial tenants, as landlords seek to pass through their increased liability (where permitted by law) and we may see this point brought up in many lease negotiations going forward.

This content has been provided by a third party and does not represent the views or opinions of Australian Property Investor Platform Pty Ltd.

Investor Partner Group, Property Tax, land tax, Queensland, investment, expenses, tax, Land Tax Act 2010 (Qld), Revenue Legislation Amendment Act (Qld) 2022, Property Investors, Property Investment Advice, Tax advice, Property Taxation, states, interstate investment, Interstate Buyers, Case Study, Queensland Revenue Office, Commercial Property, Residential Property, lease, Negotiations

29 Perth suburbs exceed 10 per cent price growth in 2022

Mount Hawthorn, just north of the CBD, led a list of 29 Perth suburbs that experienced median house price growth above 10 per cent so far in 2022, while 56 recorded growth in August.

By Damian Collins, President, REIWA | 31-8-2022 | Residential

https://www.apimagazine.com.au/news/article/29-perth-suburbs-exceed-10-per-cent-price-growth-in-2022

Twenty-nine Perth suburbs have recorded median house sale price growth of more than 10 per cent during the 2022 calendar year to date.

Mount Hawthorn experienced the strongest growth, with its median increasing 16.3 per cent to $1.265 million.

North Perth came in second, with 15.8 per cent growth, followed by Warwick (14.8 per cent growth), Carine (14.3 per cent growth) and Iluka (14.1 per cent growth), while the Fremantle area continues to perform well.

Rank Suburb Median house sale price Price growth 2022 to date 1 Mount Hawthorn $1.265 million 16.3% 2 North Perth $1.15 million 15.8% 3 Warwick $680,000 14.8% 4 Carine $1.02 million 14.3% 5 Iluka $1.027 million 14.1% 6 East Fremantle $1.475 million 13.5% 7 Mullaloo $940,000 13.2% 8 Attadale $1.537 million 13.0% 9 Subiaco $1.625 million 13.0% 10 Madora Bay $610,000 13.0% 11 Sinagra $525,000 13.0% 12 Waikiki $423,000 12.3% 13 Mount Claremont $1.74 million 12.3% 14 Karrinyup $1.065 million 11.9% 15 Cottesloe $2.85 million 11.8% 16 Two Rocks $447,000 11.7% 17 Padbury $670,000 11.7% 18 West Leederville $1.42 million 11.6% 19 Sorrento $1.283 million 11.6% 20 Riverton $736,500 11.2% 21 Gwelup $1.1 million 11.1% 22 Silver Sands $525,000 10.5% 23 Shoalwater $530,000 10.4% 24 Rivervale $612,500 10.4% 25 Midland $358,500 10.3% 26 Hammond Park $568,000 10.3% 27 Craigie $548,750 10.2% 28 Mount Helena $595,000 10.2% 29 Edgewater $642,500 10.1%

*Data is for suburbs with 28 or more annual house sales to 31 July 2022.

August also delivered median house sale price growth for 56 Perth suburbs, despite CoreLogic’s Perth home value index declining 0.2 per cent.

REIWA President Damian Collins said while the overall Perth market had seen prices grow 4.2 per cent between 1 January and 31 July, there were a considerable number of suburbs that had far exceeded that figure.

"These 29 suburbs have experienced substantial price growth in a relatively short period of time, which is very impressive – especially when you factor in the four rate rises since May.

"It will be interesting to observe how they perform for the remainder of the year and whether they can sustain the momentum of this growth trajectory,” Mr Collins said.

Further analysis revealed an additional 105 Perth suburbs had seen price growth of five per cent or more during the 2022 calendar year to date.

"REIWA agents on the ground continue to report solid market conditions, and this is reflected in the large number of suburbs that have seen strong price growth in 2022,” Mr Collins said.

“While interest rate rises will naturally have some impact on our local market, West Australians are the best placed in the country to manage the costs of servicing a loan.

“Not only do we have the most affordable housing in the country and a strong economy and jobs market, but we also have a housing shortage and growing population.

“While there may be some fluctuation month to month, all these factors point to Perth’s current growth cycle continuing.”

Property prices among Perth's best performing suburbs shot up by more than 30 per cent in the just completed financial year.

Prestige suburbs dominate the top 10 in the current list but many affordable suburbs are also generating strong capital growth, including Midland, Sinagra, Shoalwater and Craigie.

August’s top performers

REIWA President Damian Collins said a minor dip in the home value index was always a possibility given the interest rate environment, but that Perth was holding up very well overall – particularly in comparison to other capital cities around the country.

“We anticipate there will be fluctuations month-to-month in the overall Perth figure as buyers adjust to interest rates rising, however Western Australia’s strong economy, growing population and housing shortage point to the current growth cycle continuing.

“At a suburb level, reiwa.com data reflects feedback from REIWA agents who continue to report fierce competition for properties and good outcomes for sellers on the ground.

The five suburbs to record the biggest increase in price during August were Maida Vale (up 3.1 per cent to $593,750), Cooloongup (up 2.6 per cent to $370,000), Hillarys (up 2.5 per cent to $1.005 million), Southern River (up 2.2 per cent to $625,000) and Orelia (up 1.9 per cent to $327,500).

Other suburbs to perform well for median house sale price growth were Stirling, Seville Grove, Woodvale, Yanchep and Girrawheen.

![]()

![]()

![]()

![]()

![]() Damian Collins , President | REIWA

Damian Collins , President | REIWA

Damian owns a multi-million dollar property portfolio and as the founder of Momentum Wealth he applies his many years of experience to help our clients accelerate their wealth creation. His own carefu…

Perth, Mount Hawthorn, prices, Property Market, Real Estate, Perth Property Market, House Prices, median house prices, median, Damian Collins, REIWA, suburbs, Interest Rates, affordability,

Is this just the start of bigger price falls for Brisbane?

Brisbane's meteoric price rises are falling back to earth, so is this the start of a major tumble or just a minor correction?

By Melinda Jennison, Buyers Agent, Streamline Property Buyers | 3-9-2022 | Residential

Traditional Queenslander timber houses are built for flood protection, but are they safe from a property price storm?

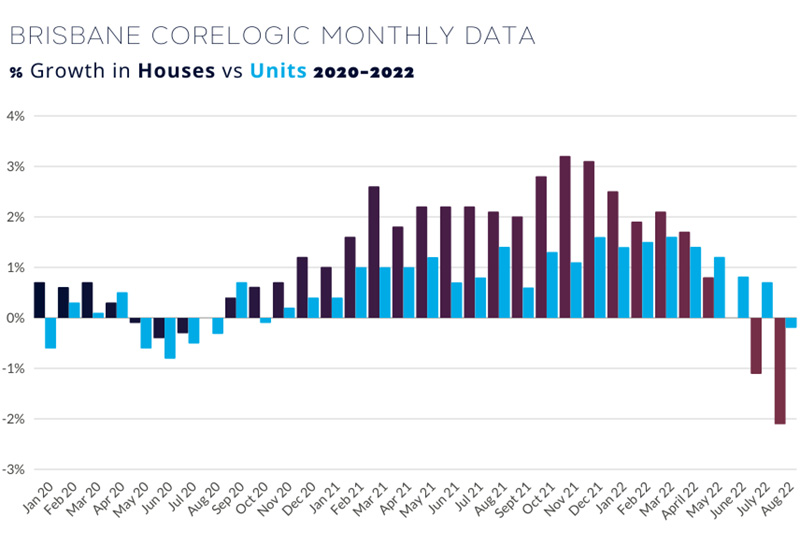

For the first time in more than two years, negative growth has been recorded in both the house and unit market across Greater Brisbane.

The latest CoreLogic Hedonic Home Value Index findings have confirmed that Brisbane house prices peaked in June 2022 and unit prices in July 2022.

Are these price adjustments the start of large falls in the months ahead, or is this simply an adjustment while buyers wait for more confidence to return to the market?

The weaker results, especially in the house market in Brisbane, accelerated during August compared to the July results.

Being mindful that this data reflects settled sales, what this tells us is that throughout July we saw a large change in buyer and seller behaviour.

This was at a time when consumer sentiment reached new lows that were comparable to other major shocks, such as the Global Financial Crisis and the onset of the Covid-19 pandemic.

A large number of buyers were fearful and taking a stance and sat on the sidelines rather than participate in active bidding on properties.

Pre-approved buyers were having to determine if their borrowing capacity had been eroded due to the rate rises that were occurring each month, which meant some buyers were simply unsure of what they could lend so were not in a position to buy.

During times of change and uncertainty, such as the current interest rate cycle, buyers tend to take a wait and see approach. Sellers also often sit out of the market waiting to see signs of improved confidence, unless there is a real motivation to sell.

There have been great buying opportunities recently, whereby sellers have been motivated and therefore willing to meet the market.

Some of these vendors had already bought elsewhere, so they needed to sell. Others were deceased estates and “quiet” sales, which included divorcees. When there is a motivated vendor, they are usually prepared to meet the market. When buyers are nervous, they tend to offer less and because of this there have been opportunities to buy quality properties for a good price.

However, we have also seen many properties not sell throughout Brisbane.

The gap between buyers and sellers does not seem to converge, and when there is no real motivation to sell, the days on market simply trends higher. These properties do not become part of the data that records property price trends.

Flight to quality

Demand for properties that have impacts such as flood or overland flow, or properties on main roads (for example) have definitely softened.

Sales agents are finding these properties a little more difficult to sell as buyers have become pickier in relation to what they want to buy, or they are pricing in a value deduction for the impacts.

During 2021, these types of properties were just as popular as everything else – there was a buyer for everything but this is no longer the case.

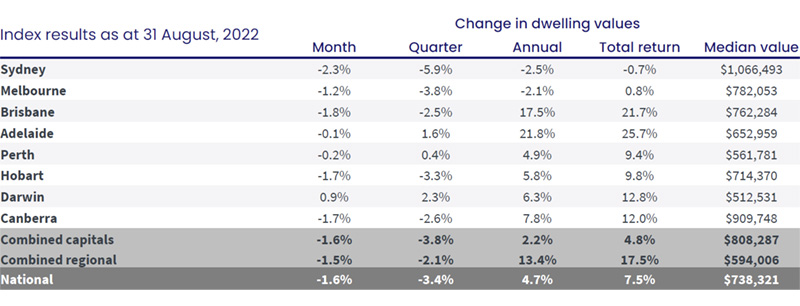

Brisbane dwelling values declined 1.8 per cent throughout August, according to the CoreLogic Hedonic Home Value Index. The median value for all dwellings across Greater Brisbane is now $762,284, which is $19,556 less than a month ago.

The rate of decline was larger in the house sector, with falls in the median value of 2.1 per cent throughout August. The median value for a house in all of Greater Brisbane is now $864,149, which is $20,187 less than last month.

Of course, this does not mean a house purchased four weeks ago is suddenly worth 2.1 per cent less than what was paid.

Every property has its own level of demand and therefore reaches its own level of value based on previous comparable sales and also the quality of what buyers are wanting.

Quality houses that are well located are still highly sought after and achieving strong prices. There appears to be a shift towards quality once more and demand is still strong for high quality homes.

Units in Brisbane have fallen very slightly over the month with a reduction of 0.2 per cent in the median value, which now sits at $501,396. This is $3,124 lower than last month.

Rents on the rise

Rental rates remain strong in Brisbane due to the low number of rental properties available, evidenced by vacancy rates that continue to hover at record lows. In July there were just 2,474 properties for rent throughout Brisbane, with a vacancy rate of just 0.7 per cent.

With very limited supply of rental accommodation, it is not a surprise that rents are still rising in Brisbane.

The annual change in housing rents increased 14.1 per cent, whereas for units the annual change was 10.7 per cent.

Brisbane still leads the capital cities throughout Australia for the largest growth in rents over the last 12 months.

While this provides some relief for landlords dealing with rising interest rates, it is not good news for tenants.

There are so many instances where properties are still receiving rental applications prior to an inspection taking place, and in most cases where a rental property is appropriately priced, there are multiple applications received from tenants.

Due to the slowdown in property prices and the continued growth in rents, gross investment yields continue to recover.

The median gross yield for Brisbane houses has increased from 3.4 per cent last month to 3.6 per cent now and for units the median gross rental yield has increased from 4.7 per cent last month to 4.8 per cent at the end of August.

These higher yields are starting to offset the increasing holding costs for investors with Brisbane assets.

While interest rates continue to rise, eroding the borrowing capacity of property buyers, and inflation continues to put pressure on household expenses, it is reasonable to expect the demand of property to remain suppressed.

It is also reasonable to expect that once inflation is under control, interest rates will find their new point and buyers will regain their confidence.

At that time we expect the buyers who have been sitting on the sidelines will re-enter the market and the depth of buyers tips Brisbane back into a sellers’ market.

![]()

![]()

![]()

![]()

![]() Melinda Jennison , Buyers Agent | Streamline Property Buyers

Melinda Jennison , Buyers Agent | Streamline Property Buyers

From a very young age I developed an interest in real estate because my parents were property investors, so I learnt a lot from the conversations that we often had growing up. I have been fortunate to…

Brisbane, Melinda Jennison, housing, houses, units, apartments, Property Prices, Property Market, Brisbane Property, CoreLogic Hedonic Home Value Index, confidence, House Price Falls, pre-approval, divorce, Distressed Sales, flood, rent, Landlords, median, Vacancy Rates, Interest Rates

Subscribe to property

investor updates

Get the latest property investment news

delivered free to your inbox each week.

Featured Articles

- Interest rates on an all-night bender while prop… 7-9-2022 | Finance

- Another interest rate double hike from aggressiv… 6-9-2022 | Finance

REIA faces tough sell in calling for end to stam… 6-9-2022 | Tax

REIA faces tough sell in calling for end to stam… 6-9-2022 | Tax - Geelong Cats fan on clawing through building ind… 5-9-2022 | Expert In Focus

- As one Sydney construction mega project ends, an… 2-9-2022 | Development

Latest News

- Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance

- Another interest rate double hike from aggressive RBA 6-9-2022 | Finance

REIA faces tough sell in calling for end to stamp duty 6-9-2022 | Tax

REIA faces tough sell in calling for end to stamp duty 6-9-2022 | Tax

8 things you need to get a home loan

Property Stamp Duty Cost in Queensland Australia

Property Stamp Duty Cost in Queensland Australia

So you’ve applied for conditional approval and you’ve found your dream home. But before you get a home loan there are certain things you’ll still need. We explore what they are and what difference they’ll make to your loan application.

Get expert help to

secure your home loan

From applying to buying, Mortgage Choice brokers are with y

So you’ve applied for conditional approval and you’ve found your dream home. But before you get a home loan there are certain things you’ll still need. We explore what they are and what difference they’ll make to your loan application.

Get expert help to

secure your home loan

From applying to buying, Mortgage Choice brokers are with you every step of the way.

With Mortgage Choice, you're never a loan.

![]()

1. Income

First and foremost, a lender will want to know that you have the capacity to repay any loan they give you. If you’re an employee they’ll usually ask you to prove this by providing payslips, bank statements showing your salary being deposited, or a letter from your employer. If you’re self-employed they’ll ask for your accountant’s details and your last two years of financial statements, as well as your personal tax return and company tax return, if you have one.

If you receive money from other sources – such as rental properties, shares or government payments – you’ll also need to provide evidence of this.

2. Evidence of what you own

At this stage, a lender will always want to see evidence of the assets you hold. This may include your superannuation balance, bank account details and a list of any shares, property or other assets you own.

Some lenders will also want to see that you have a history of saving money. That’s because they believe having the discipline to acquire “genuine savings” means you’re more likely to have the financial discipline needed to meet your ongoing repayments. Each lender will have its own definition for what qualifies as genuine savings and how long you need to have held onto the money for before applying for a loan. If you use a mortgage broker, they’ll be able to guide you through this process, letting you know exactly what you need to provide.

3. A sound credit history

All lenders will always look at your credit history before they provide you with finance. This usually comes down to getting details of your credit score. Your credit score is a mark out of 1,000 and is based on your history of paying loans and bills, as well as how often you’ve applied for credit. This includes taking into account all of your credit cards, even if you don’t owe money on them, as well as details of any other debts you have. If you have ever been declared bankrupt or have any judgments against you, this can have a serious impact on your credit score.

4. Your expenses outside of the home loan

A lender will also take into account your living costs. This includes providing details of what you spend on groceries, eating out and other day-to-day expenses, as well as ongoing costs such as utilities, childcare or education, insurance premiums and more. They will also factor in any money that you need to keep paying on accommodation after you buy the property, such as rent or another mortgage. The easiest way to present this information to a lender is in the form of a monthly budget.

5. Details of any gifts, grants or exemptions

If a family member or friend is helping you buy the home, be prepared to provide the lender with evidence of this. This may be by providing evidence of the money in your bank account or handing over a signed letter showing evidence of the loan or gift. You should also have details of any grants or exemptions you’re eligible for, such as any First Home Owners Grants or Exemptions that apply in your State or Territory.

6. Details of the property you’re purchasing

Before you’re given your home loan, your lender will usually ask for a copy of the front page of the signed contract for sale. If you’re building they may also want to see a fixed price builder’s contract and approved construction plans. Often, a lender will organise a valuation of the property you’re purchasing, particularly if you don’t have a large deposit.

7. Identification

Finally, a lender will always need formal identification, such as a passport, driver’s licence or other photo ID. If you don’t have these, you may be able to provide an original birth certificate, Medicare card or some other forms of identification.

8. Be more certain of what you can borrow with a home loan calculator

Before you apply for a loan, it’s always best to have some degree of certainty about how much you can borrow. The easiest way to do that is by using a home loan calculator. Using a tool such as this is almost always an important first step in finding out what you can afford and kicking off your search for a property on the right foo

Compare Home Loans

https://www.realestate.com.au/home-loans/compare/t.

Calculators

https://www.realestate.com.au/home-loans/calculators

Mortgage Calculator

https://www.realestate.com.au/home-loans/mortgage-calculator?cid=cid:hub:quick-link

We’ve made it easy for you to better understand your finances with our handy home loan calculator. By working out your estimated loan amount, monthly repayments and upfront costs, you can enjoy the confidence of knowing what you can afford.

You can also save this data to your realestate.com.au profile, so that when you find a property you like, you can see how it might fit with your finances and impact your current lifestyle.

Estimate your borrowing power

Our buying power calculator gives you an idea of the maximum you could spend on a property, in minutes.

https://www.realestate.com.au/home-loans/borrowing-power-calculator/#/?cid=cid:hub:quick-link

Refinance Calculator

Calculate your potential savings when switching home loans. Unlock equity in your home to renovate, buy, or invest

https://www.realestate.com.au/home-loans/refinance-calculator?cid=cid:hub:quick-link

Rent to Buy

https://www.realestate.com.au/home-loans/reverse-rent-calculator?cid=cid:hub:quick-link

Estimate how much you may be able to borrow if you put your current rental payments towards paying off a home loan.

Estimate how much you may be able to borrow if you put your current rental payments towards paying off a home loan.

Another interest rate double hike from aggressive RBA

In its desperate bid to suppress rampant inflation, borrowers have been hammered with yet another super-sized interest rate increase from the Reserve Bank of Australia.

By Craig Francis | 6-9-2022 | Finance

https://www.apimagazine.com.au/news/article/another-interest-rate-double-hike-from-aggressive-rba

The Reserve Bank of Australia has hit homeowners with a fifth consecutive monthly interest rate hike, again unloading with a 50 basis point (0.5 per cent) increase that will stretch millions of household budgets.

In announcing its decision the RBA Board made it clear that the new official cash rate of 2.35 per cent is set to rise further before the year is out.

“The Board expects to increase interest rates further over the months ahead, but it is not on a pre-set path,” the statement by Philip Lowe, Governor, Reserve Bank, noted.

“The size and timing of future interest rate increases will be guided by the incoming data and the Board's assessment of the outlook for inflation and the labour market.

The Board is committed to doing what is necessary to ensure inflation in Australia returns to target over time.”

The cash rate setting is now at the highest level since January 2015, but still slightly below the pre-Covid decade average of 2.56 per cent.

Property impact

This rise is highly likely to be passed on in full to household mortgage holders.

Housing markets have reacted negatively to the rate hiking cycle, with capital city housing values down 4.5 per cent since peaking shortly after the first lift in the cash rate on 5 May.

It is reasonable to expect higher interest rates will flow through to less housing activity as borrowing capacity diminishes and sentiment remains low, placing further downwards pressure on housing prices.

CoreLogic’s estimate of national home sales over the three months to August was tracking 14.8 per cent lower than the same period a year ago, highlighting that housing demand has already been dented by the recent cycle of rate hikes.

“As we move into spring, there is good chance buyer demand will continue to taper as interest rates rise, leading to higher advertised inventory levels amid more challenging selling conditions,” CoreLogic Research Director, Tim Lawless, said.

RateCity.com.au analysis shows the impact this hike will have once it is passed on by lenders:

Owner-occupiers:

- 5.11 per cent will be the average existing customer variable rate for owner-occupiers.

- Under 4 per cent will be a competitive variable rate for owner-occupiers paying principal and interest.

- About a dozen lenders are likely to have variable rates under 4 per cent.

Investors:

- 5.46 per cent will be the average existing customer variable rate for investors.

- Under 4.30 per cent will be a competitive variable rate for investors paying principal and interest.

- About a dozen lenders will have investor variable rates under 4.30 per cent.

For a typical housing mortgage of $500,000, Tuesday’s (6 September) increase will add $2,500 in annual interest payments, or $208 per month. The cumulative increase of 2.25 per cent so far this year will have added $11,250 in annual interest payments, or $937 per month in additional interest payments.

Finance scramble

Steve Douglas, Executive Chairman, SMATS Group, labelled the supersized interest rate hike as extremely disappointing and unnecessary.

“Given we have had quick and significant rises already, I believe a wait-and-see position to assess the impact would have been a more sensible option given the current environment.

“That said, the base rate still remains historically low, and hopefully many have taken advantage of the low fixed rates that were on offer during the past two years.

“Some level of sensibility is now required, so hopefully rate rises take a pause for a while and allow the economy to settle,” Mr Douglas said.

Julie Toth, Chief Economist of online property exchange network PEXA, said the RBA move reflects elevated inflation pressures in Australia and globally, supply shortages across the construction industry and in other key sectors, and an extremely tight labour market.

“Australia is experiencing historically low unemployment and underemployment rates and – for the first time recorded – fewer unemployed people than advertised job vacancies nationally.

“Today’s announcement is likely to continue the surge of Australians exploring their refinancing options, as mortgage-holders seek out discounts and cheaper options for their home loans from their existing lender or new sources,” Ms Toth said.

Compare Club CEO, Lance Goodman, said the persistent interest rate increases were now making an impact on the housing market, with lenders continuing to tighten the borrowing capacities for buyers and homeowners.

“It would seem more people are holding rather than buying and waiting to see where the market bottoms out, which is likely to be in some ways contributing to further falls in property values, given the reduced demand,” Mr Goodman said.

“The good news is, we're still in a buyers’ market, so first-home buyers can benefit.”

Not their problem

A consideration of housing prices is not part of the RBA’s mandate, which has made it clear it is prepared to look through the peripheral noise of falling home values, focusing instead on inflation and labour market conditions.

“Inflation in Australia is the highest it has been since the early 1990s and is expected to increase further over the months ahead,” Mr Lowe said on Tuesday.

“Global factors explain much of the increase in inflation, but domestic factors are also playing a role.

“There are widespread upward pressures on prices from strong demand, a tight labour market and capacity constraints in some sectors of the economy.”

Mr Lowe acknowledged higher inflation and interest rates were putting pressure on household budgets, with the full effects of the new rates yet to be felt in mortgage payments.

“Consumer confidence has also fallen and housing prices are declining in most markets after the earlier large increases (but) working in the other direction, people are finding jobs, gaining more hours of work and receiving higher wages.

“Many households have also built up large financial buffers and the saving rate remains higher than it was before the pandemic.

“The Board will be paying close attention to how these various factors balance out as it assesses the appropriate setting of monetary policy.”

Buffer or buffeted

While Mr Lowe points to data showing loan arrears are low and the saving rate remains higher than before the pandemic, many households will be feeling the pinch.

The value of new owner-occupier loan commitments fell 7.0 per cent in July 2022, while new investor loan commitments fell 11.2 per cent. Further falls appear likely as the latest rate hikes take effect.

Research from lender group Aussie found that almost one in five Australians with mortgages are dealing with ‘significant mortgage stress’, and a further four in five confirmed the rising cash rate and upward cost of living is placing unwanted tension on their household.

Another new survey shows 40 per cent of Australians report the cost-of-living and personal debt are causing them elevated distress compared with this time last year.

Suicide Prevention Australia’s annual State of the Nation report reveals 70 per cent of Australians have experienced elevated distress beyond their normal levels compared with this time last year.

Cost-of-living and personal debt was the lead cause (40 per cent), and was higher for women (44 per cent) than men (36 per cent). This is despite near-equal levels of overall elevated distress as between women (71 per cent) and men (69 per cent).

Suicide Prevention Australia, CEO, Nieves Murray said further economic turbulence could prove challenging.

“For example, the issue of cost-of-living and personal debt is ranked the biggest risk to rising suicide rates over the next 12 months both by the public (68 per cent) and by the suicide prevention sector (74 per cent).”

As well as enjoying a career as an international news journalist and editor with major international news organisations such as CNN (London and Hong Kong), Financial Times (UK), South China Morning …

interest rates, RBA, RBA Monthly Meeting, inflation, wages, Property Prices, cost of living, Philip Lowe, borrowers, SMATS Group, Steve Douglas, ratecity, CoreLogic, Tim Lawless, fixed rate loans, variable rate loans, mortgages, banks

Subscribe to property

investor updates

Get the latest property investment news

delivered free to your inbox each week.

Featured Articles

- Interest rates on an all-night bender while prop… 7-9-2022 | Finance

- REIA faces tough sell in calling for end to stam… 6-9-2022 | Tax

- Geelong Cats fan on clawing through building ind… 5-9-2022 | Expert In Focus

- Is this just the start of bigger price falls for… 3-9-2022 | Residential

- As one Sydney construction mega project ends, an… 2-9-2022 | Development

Latest News

- Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance

- REIA faces tough sell in calling for end to stamp duty 6-9-2022 | Tax

Geelong Cats fan on clawing through building industry's tough times 5-9-2022 | Expert In Focus

Geelong Cats fan on clawing through building industry's tough times 5-9-2022 | Expert In Focus

Continue reading Finance ArticlesView All Finance Articles

Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance  Government dismisses Greens call for two-year rent freeze 25-8-2022 | Finance

Government dismisses Greens call for two-year rent freeze 25-8-2022 | Finance  Another big leap takes interest rates to six-year high 2-8-2022 | Finance

Another big leap takes interest rates to six-year high 2-8-2022 | Finance  Great Australian property dream being put to sleep 31-7-2022 | Finance

Great Australian property dream being put to sleep 31-7-2022 | Finance  Soaring inflation offers no reprieve to mortgage holders 27-7-2022 | Finance

Soaring inflation offers no reprieve to mortgage holders 27-7-2022 | Finance  RBA to be scrutinised in first review for decades 20-7-2022 | Finance

RBA to be scrutinised in first review for decades 20-7-2022 | Finance

Busting three myths around commercial property investment

Three persistent myths continue to deter prospective investors from commercial property but with some due diligence applied, they are exposed as fictions.

By Scott O'Neill, Director, Rethink Investing | 2-9-2022 | Commercial Property

Properties in high-demand, low-supply areas will always be snapped up by tenants.

Despite seeing exceptional capital growth and strong market conditions in many sectors over the past few years, there are still people that talk about all the possible downsides to commercial property compared to residential.

Like any investment there are risks in commercial property, however, those that criticise it, more often than not, don’t understand it as an asset class and don’t know how to mitigate these risks through due diligence.

Let’s take a closer look at three common reasons people avoid buying commercial compared with residential and why that’s wrong:

‘Long vacancies are inevitable’

This is probably the main reason people won’t invest in commercial property and one of the biggest myths.

The truth is vacancies can be long for poor-quality assets but are generally shorter for high-grade, well-located properties.

Investors need to carefully assess all relevant factors, such as the quality of the building, location, rent levels and the state of the general market around it. Getting the due diligence right will help ensure that the property won’t stay vacant for long.

Properties in high-demand, low-supply areas will always be snapped up by tenants. If you purchase a commercial property in a poor location and the building is in disrepair, then of course the vacancy periods will be longer. It’s all about buying good-quality properties with strong relatability potential.

Many leases have minimum vacate notice periods in the contract. If you are notified by your tenant six months out, then you have six months’ rent coming in while you search for a new tenant and in many cases, tenants will notify you well over a year in advance. As you can see, commercial leasing is very different from residential, where tenants can just pick up and leave with a day’s notice.

‘Low capital growth’

This couldn’t be further from the truth. We’ve seen commercial properties double or even triple in value over a 10-year period. The question is how to improve your chances of buying a property that will get better growth than others?

As in the residential market, there are plenty of factors that can contribute to capital growth, including good location, scarcity factor, infrastructure improvements, population growth, tightening vacancy rates renovations or falling interest rates.

Now guess what causes growth for commercial property? All the above! Because as in the residential space, the commercial market also responds to these economic improvements. The one big difference is that commercial property has more of its growth attached to its rental income. So, increasing or improving the lease quality will have a larger overall impact on the commercial asset value.

‘Fewer value-add opportunities’

It’s completely possible to raise long-lasting value on a commercial property if you know what to do. Unlike residential properties, where it’s all about improving the liveability of a property, in commercial the numbers do all the talking.

Because much of the value of a commercial property is tied to its rental income, finding properties that are under-rented can be the path to easy equity gains.

For example, a 500/m2 metre property renting for $100,000 per annum is valued at $200/m2. If the market rent is $240/m2, the property is under-rented by 20 per cent.

In that case, if you have a plan and the means to get the rent back up to market level, your income will be 20 per cent higher. And this could increase the value of the commercial property by 20 per cent, assuming you bought it at the correct yield from day one.

Another value add is strata titling or subdividing the property. This adds value because you can sell or rent smaller sections at a higher per-square-metre rate.

For example, a 1000sq metre warehouse might rent for $100/m2. But five 200sq metre warehouses could potentially rent at $130/m2. Essentially, you are reversing the ‘economies of scale’ in your favour, and your value could increase by 30 per cent due to the higher rent per square metre. There are other value-adds too, including renovating, lengthening leases, rezoning and developing.

When you purchase a high-quality commercial asset, do your due-diligence and employ a solid positively geared strategy, your commercial investment will far exceed anything you would have known in the residential world.

![]()

![]()

![]()

![]()

![]() Scott O'Neill , Director | Rethink Investing

Scott O'Neill , Director | Rethink Investing

Scott and Mina O’Neill are co-authors of best-selling commercial book; Rethink Property Investing. They are also the founders of Rethink Investing, Australia’s number one buyers’ agency for commercial…

commercial, Commercial Property, Scott O'Neill, Property Investment Advice, rent, vacancy, assets, Capital Growth, commercial lease, Value-Add, Population Growth, Profitability, Buildings, investment, Property Investors

Property monthly price falls biggest since 1983

The biggest property price drop in almost 40 years is the fourth successive monthly market decline and there’s no sign of an immediate turnaround.

By Craig Francis | 1-9-2022 | Residential i

https://www.apimagazine.com.au/news/article/property-monthly-price-falls-biggest-since-1983

While prices remain above pre-Covid levels, storm clouds are opening up above the Australian property market after years of sustained price.

Australia’s property price declines are accelerating and spreading, with August delivering the sharpest monthly retreat since 1983.

Down 1.6 per cent over the month, CoreLogic’s national Home Value Index (HVI) has clocked up its fourth consecutive month of price falls.

Unless you were a homeowner in Darwin or regional South Australia, there was nowhere to hide.

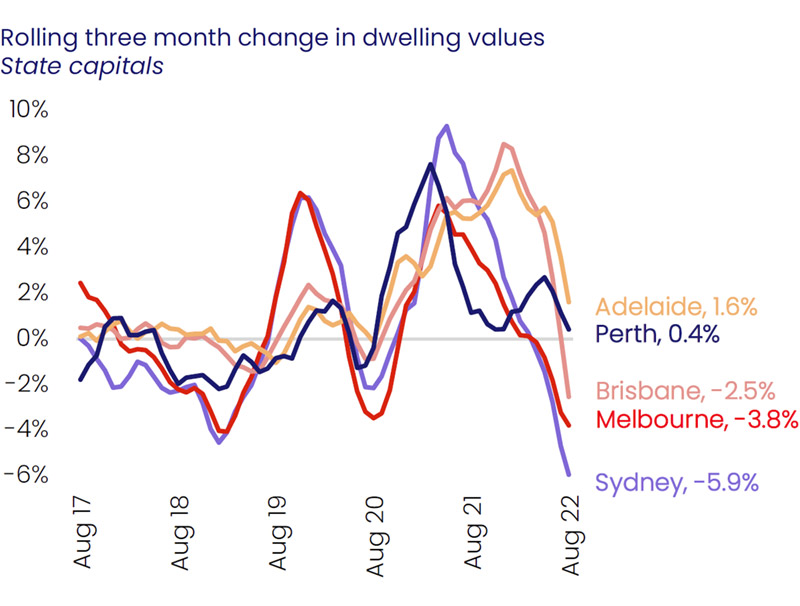

Sydney continued to the lead the downswing, with values falling 2.3 per cent over the month, however weaker conditions in Brisbane accelerated sharply through August, with values falling 1.8 per cent.

CoreLogic’s research director, Tim Lawless, said Brisbane’s shift into decline had been acute after almost two years of sustained growth due to record high internal migration and relative affordability.

“It was only two months ago that the Brisbane housing market peaked after recording a 42.7 per cent boom in values.

“Over the past two months, the market has reversed sharply with values down 1.8 per cent in August after a 0.8 per cent drop in July,” Mr Lawless said.

REIQ CEO Antonia Mercorella said the Real Estate Institute of Queensland’s recently released quarterly results showed Queensland’s soaring property market growth has started to show signs of calming after a period of unsustainable growth.

Across the 41 regional sub-regions analysed nationally, only seven areas recorded a rise in housing values in August, including the northern suburbs of Adelaide (0.9 per cent), Perth’s North East and Mandurah to the south (0.6 per cent/0.5 per cent) and the Coffs Harbour-Grafton region (0.6 per cent).

Regional retreat

Regional Australia’s spell as the price growth alternative driven by a flight to pandemic lifestyle relief has also come to a shuddering halt.

After recording significantly stronger appreciation through the upswing, the fall in regional dwelling values is catching up with the capital cities. Regional home values were down 1.5 per cent in August compared with a 1.6 per cent fall in values across the combined capitals.

Between March 2020 and January 2022 regional dwelling values surged more than 40 per cent, compared with a 25.5 per cent rise for the combined capitals.

“The largest falls in regional home values are emanating from the commutable lifestyle hubs where housing values had surged prior to the recent rate hikes,” Mr Lawless said.

“Over the past three months, values are down 8.0 per cent across the Richmond-Tweed, 4.8 per cent across the Southern Highlands-Shoalhaven market and 4.5 per cent across Queensland’s Sunshine Coast.”

No relief in sight

The prospects of the national property market dodging a fifth successive drop appear slim.

Financial markets are expecting the Reserve Bank of Australia (RBA) to increase official interest rates again next week by 0.5 percentage points.

A fifth straight month of rate rises, most of them double sized, would only serve as more negative sentiment for the real estate market.

As the spring selling season begins, more properties are expected to come onto the market at a time of relatively weak demand, which is likely to ensure prices keep falling.

Selling conditions across Australia’s unit markets have continued to weaken after a period of outperforming house markets.

Builders are feeling as much pain as property owners, with the total number of dwelling approvals falling a whopping 17 per cent in July.

Prices well above pre-Covid

Despite the recent weakness, housing values across most regions remain well above pre-COVID levels.

Housing affordability has barely improved despite the property market downturn, new research revealed.

The time it takes to save for a home deposit across the combined capital cities fell by a negligible 11 days to 11.11 years in the three months to June 2022, the latest ANZ/CoreLogic Housing Affordability Report found.

It’s barely different in regional areas.

It takes 10.7 years to save for a deposit in the regions as of the June quarter, up from 10.4 years three months earlier.

Households now spend 44 per cent of their income on repaying a new home loan, the report estimates. Anything above 30 per cent is regarded as entering into the domain of experiencing mortgage stress.

That is the highest level since June 2011 and up from 40.4 per cent in the previous quarter.

Renters are in just as much pain, with the typical tenant paying 30.9 per cent of income on rent, up a 0.6 per cent on the previous quarter.

Home values in all capital cities and rest-of-state regions, bar Melbourne, still remain 15 per cent or more above the levels recorded in March 2020, implying most homeowners have a significant equity buffer before their home is likely to be worth less than what they paid.

“A 15 per cent peak to trough decline would roughly take CoreLogic’s combined capitals index back to March 2021 levels,” Mr Lawless said.

“Additionally, many homeowners would have had at least a 10 per cent deposit and paid down a portion of their principal, the risk of widespread negative equity remains low.”

As to whether this downturn was different to others or ending abruptly, Mr Lawless said he expects it will continue to play out through the remainder of the year and possibly into 2023.

“It’s hard to see housing prices stabilising until interest rates find a ceiling and consumer sentiment starts to improve,” he said.

“From current levels, interest rates are likely to increase by at least another 75 basis points and there is a good chance advertised stock levels will accumulate through the spring selling season, providing more choice for buyers and adding further downwards pressure on housing values.”

As well as enjoying a career as an international news journalist and editor with major international news organisations such as CNN (London and Hong Kong), Financial Times (UK), South China Morning …

Property Prices, Prices Fall, House Prices, apartments, units, House Price Falls, Home Value Index, CoreLogic, Median Home Values, Capital Growth, Capital Cities, Perth, Darwin, Melbourne, Sydney,

As one Sydney construction mega project ends, another begins

Two new Sydney mega projects at opposite ends of their journeys will transform significant parts of Sydney, with the new Sydney Football Stadium opened Friday and work beginning on the $1.2 million Victoria Cross Tower in North Sydney.

By Craig Francis | 2-9-2022 | Development

Two new megaprojects promise to transform their respective parts of Sydney.

After over four years of construction, the new Sydney Football Stadium finally opened on Friday night (2 September) in a double-header of rugby league.

Meanwhile, Lendlease has announced this week that construction is set to begin on its flagship $1.2 billion commercial building and retail precinct in North Sydney, Victoria Cross Tower.

Both projects will be crowd-pullers.

Victoria Cross Tower will accommodate up to 7,000 workers across approximately 58,000 square metres of high-tech, premium space for office and retail use, while the stadium’s $874 million rebuild has resulted in a capacity of 42,500.

The stadium is officially the home of rugby league’s Roosters, Waratahs (Super Rugby union) and Sydney FC (A-League soccer), with the South Sydney rugby league team also keen to share home billing from next season.

Standing ovation

The new stadium, which stands next to the famous Sydney Cricket Ground (SCG), was delivered 20 per cent over budget but on time, quite a feat in today’s troubled building industry environment. It cost the equivalent of $106 for every man, woman and child in NSW.

The city’s premier rectangular stadium replaces the original Sydney Football Stadium, located at Moore Park and features three levels of seating on either side of the playing arena, steep seating angles, which provide unrivalled views of the field and a 360-degree open concourse inside and outside the venue, which includes contemporary bar and dining options, modern bathrooms and stunning corporate and member facilities.

Streamlined interior of the new Sydney Football Stadium

The innovative and iconic new build was designed by Cox Architecture.

A contractor on the project, Stuart Farrelly, NSW Commercial Sales Manager, CSR Gyprock, said it had to take into account the unique parameters of the football stadium.

“Moderation of the immense sound and energy output of up to 42,500 spectators was key to creating a comfortable experience and products were specified for their aesthetic and performance capabilities.

“Issues included mass volumes of people, foot traffic, noise and the numerous types of rooms requiring specific applications including wet rooms, changing rooms, media rooms, kitchens, restaurants, corridors as well as stands, the functionality and performance criteria that each product had to meet was significant, with the additional considerations of seismic and building code regulations,” Mr Farrelly said.

The promise to rebuild Allianz (the corporate naming rights holder to the new stadium) and Stadium Australia in Sydney Olympic Park was a polarising issue at the 2019 NSW state election.

Legal threats also swirled around the project but NSW Sports Minister Alister Henskens dismissed suggestions the NRL could sue NSW for reneging on the $800m promise to redevelop Stadium Australia - a condition of the competition's contract with the state government in 2018 to keep the grand final in Sydney until 2042.

That later became a deal to refurbish before everything was cancelled in 2020 as the state dealt with Covid.

"That (lawsuit) is unlikely, given nothing has happened for two years and for any specific performance suit, there would need to be a demonstration that a party has acted quickly," Mr Henskens told media.

North Sydney ‘lynchpin’

Rising above North Sydney’s newest Metro station, the 42-storey office tower will be the lynchpin for a new commercial and retail precinct as the region’s resurgence continues. Work will start before the end of the year.

Victoria Cross Station is expected to transform North Sydney’s CBD into one of the most accessible business districts in the city, cutting transit times to places like Barangaroo and Martin Place to mere minutes.

Above it, the 42-storey office tower designed by Bates Smart will be net zero carbon, powered by 100 per cent renewables.

On ground level, there will be an expansive lobby and retail laneway with more than 20 new shops and hospitality brands planned, as well as bars, restaurants and cafes.

Victoria Cross Tower is 25 per cent owned by Lendlease's flagship Australian office fund, APPF Commercial.

Victoria Cross retail laneway

Victoria Cross Tower is due to be completed in 2024, with Sydney Metro City & Southwest services set to start in the same year.

Constructing the $1.2 billion precinct will see the building rise approximately one floor each week.

The project will support around 5,000 jobs in fields such as engineering, construction and design, with 90 per cent of the workforce being local to the Sydney area.

Development in North Sydney has ramped up in recent months including, in June, Sydney-based developer Stockland Corporation winning approval for a $1.4 billion, 51-storey office tower in North Sydney.

North Sydney Council approved the development application for Affinity Place. It will be the tallest building in the lower north shore.

Deicorp expects to start work within a month on its $445-million mixed-use project to be built above a recently completed Metro station in Sydney’s north-west.

As well as enjoying a career as an international news journalist and editor with major international news organisations such as CNN (London and Hong Kong), Financial Times (UK), South China Morning …

building and construction, development, Major Projects, Project Management, Sydney, commercial, retail, sport, rugby, soccer, football, Victoria Cross Tower, Sydney Football Stadium, Allianz Stadium, Lendlease, SCG, Cox Architecture, design, Stuart Farrelly, CSR Gyprock, architecture, Energy Efficiency, renewable energy, carbon neutral, election, NSW Government, Alister Henskens, NRL, A-League, Super Rugby, Victoria Cross Station, APPF Commercial, Bates Smart, Deicorp, Affinity Place, Stockland Corporation

Featured Articles

- Interest rates on an all-night bender while prop… 7-9-2022 | Finance

- Another interest rate double hike from aggressiv… 6-9-2022 | Finance

- REIA faces tough sell in calling for end to stam… 6-9-2022 | Tax

- Geelong Cats fan on clawing through building ind… 5-9-2022 | Expert In Focus

- Is this just the start of bigger price falls for… 3-9-2022 | Residential

Latest News

- Interest rates on an all-night bender while property gets depressed 7-9-2022 | Finance

- Another interest rate double hike from aggressive RBA 6-9-2022 | Finance

- REIA faces tough sell in calling for end to stamp duty 6-9-2022 | Tax

Australian Property Investor Magazine

Property Stamp Duty Cost in Queensland Australia

Australian Property Investor Magazine

https://www.apimagazine.com.auAustralian property investment news and information for investors, homebuyers and real estate professionals – Property investment ...

https://www.apimagazine.com.auAustralian property investment news and information for investors, homebuyers and

https://www.apimagazine.com.auAustralian property investment news and information for investors, homebuyers and real estate professionals – Property investment ...

https://www.apimagazine.com.auAustralian property investment news and information for investors, homebuyers and real estate professionals

Interest rates on an all-night bender while property gets depressed

API Magazine Editor Craig Francis draws upon an old-school journalist's bar-room view of the world to assess what the current interest rate cycle and economic situation means for property prices.

By Craig Francis | 7-9-2022 | Finance

API Magazine Editor Craig Francis draws upon an old-school journalist's bar-room view of the world to assess what the current interest rate cycle and economic situation means for property prices.

By Craig Francis | 7-9-2022 | Finance

Property seems locked into an unhealthy relationship with interest rates.

The higher the latter soars, the more depressed the former becomes.

It wasn’t long ago that property was the one out dancing while interest rates sat on the floor cross-legged watching the world go by.

Interest rates clearly found their mojo and the question now on property’s lips is, when will interest rates finally settle down?

The answer seems to be that it’s midnight and interest rates still want to party until dawn, regardless of how much of a downer that puts on property.

Inflation

Inflation is the that evil friend everyone’s had that won’t let interest rates go to bed.

Any hopes that interest rates may be nearing their peak went out the window with Tuesday’s Reserve Bank (RBA) decision to raise interest rates by a double-sized 0.5 per cent for the fourth time in a row, in addition to the smaller rate rise that started it all in May.

So far, inflation has paid scant regard to the RBA despite anyone with an $800,000 mortgage having $1,000 less to spend each month.

But many sceptics of the RBA’s approach argue it might be on an interest rates bender without thinking about the possible hangover, in the form of loan delinquencies, forced property sales and heavily stressed households.

CBA’s head of Australian economics, Gareth Aird, released research showing that it takes an average of two-to-three months for an increase in the RBA’s official cash rate to be felt by mortgage holders.

So, has the RBA had time to assess the impact of it go-hard attitude?

Mr Aird went along with the party analogy.

“The RBA’s aggressive tightening is “like having five shots of vodka in an hour and saying, everything is OK but you know that it will soon have a big effect,” he said.

“I firmly believe the RBA has lifted rates too far, too quickly, and should pause to see what the effect is, otherwise, it risks driving household consumption off a cliff, crashing house prices, and driving Australia into an unnecessary recession.

“I also believe the RBA will be forced to cut rates mid next year (as) by then, the delayed impact of rate hikes will have arrived with house prices having fallen sharply, the economy stalling, and inflation declining,” he told media.

But RBA Governor Philip Lowe is having none of that and is lining the shots up on the bar.

“Inflation in Australia is the highest it has been since the early 1990s and is expected to increase further over the months ahead”.

“The Board expects to increase interest rates further over the months ahead, but it is not on a pre-set path.”

Rest of the world

Inflation is not a uniquely Australian issue.

Around the world, advanced economies are wrestling with inflation that has been stirred by easy credit, money-printing machines working through the night (or quantitative easing, as the economists prefer to call that sort of all-nighter), and pandemic stimulus packages that pump-primed the economies as business ground to a lockdown halt.

Traditionally, inflation in Australia has been the result of rising wages, and a blunt instrument like interest rates has been able to constrain runaway prices caused by cashed up workers spending freely.

But the current economic picture is markedly different.

With wages only now showing signs of emerging from hibernation and nowhere near matching inflation that sits at 6.1 per cent, it’s external factors that are driving up prices.

Philip Lowe (almost) admitted as much in his Monetary Policy Decision on Tuesday.

“The path to achieving this balance is a narrow one and clouded in uncertainty, not least because of global developments,” he noted.

“The outlook for global economic growth has deteriorated due to pressures on real incomes from high inflation, the tightening of monetary policy in most countries, Russia’s invasion of Ukraine, and the Covid containment measures and other policy challenges in China.”

But he went some way to countering the critics who said interest rates will do little to alleviate inflation that has nothing to do with how much money households have left after paying for expensive fuel and groceries and swollen mortgage repayments.

“Global factors explain much of the increase in inflation ...” – drumroll – “... but domestic factors are also playing a role.”

“There are widespread upward pressures on prices from strong demand, a tight labour market and capacity constraints in some sectors of the economy.”

He clearly believes in his primary weapon and isn't afraid to use it.

Wages

Mr Lowe also had a salutary message for anyone who thought a little wage increase might alleviate some of the financial pain.

“Wages growth has picked up from the low rates of recent years and there are some pockets where labour costs are increasing briskly.

“Given the tight labour market and the upstream price pressures, the Board will continue to pay close attention to both the evolution of labour costs and the price-setting behaviour of firms in the period ahead.”

By “pay close attention” he means rates are going up to cover any wage hikes or predatory pricing by business.

In another sign that property prices won’t be getting any favours from workers earning more money, households are not the ones benefiting from an improving economy.

Federal Government Treasurer Jim Chalmers said it out loud.

“We saw company profits reach record highs as a percentage of GDP, but real household disposal incomes fell for the third consecutive quarter by 0.5 per cent in the June quarter that meant real incomes fell again,” he said

“While there are some welcome and encouraging science that wages are starting to pick up, there is no significant measure of wages growth that tells us anything other than real wages are still falling given the high and rising inflation that we confront in our economy,” he said.

Driving home that point, data revealed almost a third of national income went to profits (32.9 per cent) while a record low share went to wages (48.5 per cent).

Where’s the party?

So, what does it all mean for property prices that were partying like it was 1999 in 2019 (and thereabouts – it was a big party)?

It’s difficult to mount a strong case that they are going to arrest their slide before interest rates curtail rampant inflation, perhaps late in 2023 – but where they bottom out in that time is unclear.

Economists say the current downturn could be the steepest and longest since the 1990s. Others point out that national property price booms last around three times longer than the downturns, so could soon bounce like partygoers in a mosh pit.

The punters for now though are a little less energetic.

They're sitting home and paying off their credit cards (debt is down by 1.8 per cent according to data released Wednesday, 7 September), refinancing their scary loans in record numbers (PEXA’s Refinance Index up by 3.7 per cent for the month to 4 September), and avoiding risky loans (APRA’s Quarterly ADI Property Exposure report reveals risky loans have come down from the record levels of December 2021).

So, first-home buyers are watching intently and saving for that elusive deposit in the face of rising rents and living pressures, buyers who were late to the party watch in dread as they creep towards negative equity and investors reassess their buy and sell strategies.